How to Get Nonprofit Status: A Director's Guide

Quick Answer: How to Get Nonprofit Status: A Director's Guide

: state incorporation, EIN, IRS 501(c)(3), and the operational habits directors need before compliance gets public. The sections below walk through practical steps, examples, and what to watch for.

For nonprofit books once you are operating, see fund accounting.

You may be staring at a good mission and a messy legal pad right now. You know the need is real, but the path to official status feels slow, technical, and easy to get wrong.

It helps to reframe the work. How to get nonprofit status isn’t just about filing forms. It’s about building an organization that donors trust, grantmakers can vet, and your board can run without chaos a year from now.

The Journey from Idea to Impact

A founder gets the call on a Tuesday. A family needs help, a school program is about to disappear, or a neighborhood project has outgrown volunteer cash and Venmo transfers. By Friday, the same founder is reading about bylaws, EINs, conflict policies, and IRS forms and wondering how any of that connects to the mission.

It connects more than people expect.

Your legal setup shapes daily operations from the start. It affects how you accept donations, how your board approves spending, how you track restricted funds, and how painful your first reporting cycle will be. Founders who treat formation as a filing project often end up rebuilding their records, policies, and workflows after approval.

Nonprofit and tax-exempt are not the same thing

These terms get blurred together early, and that causes confusion.

A nonprofit usually describes the entity you form under state law, often a nonprofit corporation. That gives the organization a legal home, a governing structure, and a way to open accounts, sign contracts, and limit personal liability.

Tax-exempt status is separate. The IRS explains the requirements for organizations seeking recognition under Section 501(c)(3) in its guidance for charitable organizations. That federal recognition is what generally allows donors to claim tax deductions for eligible gifts and tells grantmakers they are dealing with an approved charitable organization.

The distinction shows up in real life. A group can be properly formed with the state and still be months away from federal recognition. During that gap, fundraising options, grant eligibility, and donor messaging all need extra care.

Why 501(c)(3) is usually the goal

For a new public charity, 501(c)(3) status is usually the practical target because it affects funding, credibility, and reporting all at once.

The IRS expects annual information returns from most exempt organizations, and those filings become part of the public record. Donors, foundations, watchdogs, and board recruits often look at that record before they commit. Approval is not the finish line. It is the point where your administrative habits become visible.

That is why I tell founders to build for year two while they are still working on year one. If your donation tracking is improvised, your chart of accounts is vague, or board approvals live in scattered email threads, those problems will surface later in Form 990 prep, grant reporting, and audits of restricted funds.

Set up for operations, not just approval

Before filing, answer a few questions that sound administrative but have mission consequences.

- How will you track restricted gifts? Scholarship money, benevolence funds, and program grants need clean separation from general operating support.

- How will your board review finances? Reports should make sense to directors, not just your accountant or treasurer.

- How will you keep a record of decisions and activity? You will need organized minutes, donation records, grant terms, governing documents, and policy acknowledgments.

- What system will hold this information from day one? Spreadsheets and shared drives can work for a short stretch, but they break down fast once grants, acknowledgments, and annual filings start stacking up.

An integrated platform helps because it connects the legal file, board records, finances, and donor data early, before your team creates three versions of the truth in three different places. That saves time, but what's more, it cuts down the compliance problems that show up when someone tries to reconstruct a year of activity from inboxes and bank statements.

If you are still sorting out entity options before you form, how to choose a business structure gives useful context on why the nonprofit corporation model is usually the right fit. For the order of operations, this start a nonprofit checklist is a practical way to map the work before you draft filings or recruit board members.

Building Your Foundation at the State Level

A lot of founders hit this stage feeling relieved. The mission is clear, a few board members have said yes, and the federal application feels like the big hurdle. Then the state paperwork starts, and small drafting choices begin creating bigger operational problems than anyone expected.

Form the entity with your day-to-day reality in mind. In most cases, that means creating a nonprofit corporation in your state and setting up records in a way your future board, bookkeeper, and grant writer can use.

Choose a structure that supports the mission

If you’re still weighing options, a law firm overview like how to choose a business structure can help clarify why nonprofit corporation status is usually the right fit for a public charity.

That choice gives you more than a filed entity. It sets the rules for ownership, control, board authority, and asset protection. It also affects how easily you can open a bank account, adopt bylaws, apply for exemptions, and prove to funders that the organization is built to last.

A practical starting file usually includes:

- Articles of Incorporation filed with your state

- A purpose clause that matches charitable or educational activities the IRS recognizes

- A dissolution clause directing remaining assets to another qualifying exempt organization

- Foundational governance records, including bylaws and initial board actions

Founders often treat these as filing tasks. They are operating documents. If your purpose is muddy, your programs drift. If your board authority is unclear, approvals get messy. If records live in email threads and personal drives, annual reporting turns into a reconstruction project.

Write Articles the IRS can approve and your team can work from

The Articles are not just a state form. They become part of the legal record that supports your federal exemption request.

Your purpose statement should reflect what the organization will do in the first few years. Broad language may feel flexible, but it often creates avoidable questions later, especially if your early revenue, grant requests, and program descriptions point in different directions. Clear language helps with more than IRS review. It helps staff and board members stay aligned when new opportunities show up.

The dissolution clause matters for the same reason. Charitable assets have to stay in charitable use. If that clause is missing or weak, you may end up amending your formation documents before the federal filing can proceed.

I’ve seen new nonprofits lose weeks here because the corporation was formed quickly, but no one checked whether the state template included IRS-friendly language. Fixable, yes. Efficient, no.

Build bylaws for the board you can realistically run

Bylaws should answer routine governance questions before they turn into conflict. Who elects directors. How long terms last. What officers are expected to do. How meetings are called. What counts as a quorum. How conflicts of interest are disclosed and documented.

The trade-off is straightforward. Thin bylaws leave too much to improvisation. Overbuilt bylaws lock a small startup board into procedures it cannot maintain.

A healthy baseline is an independent board with enough separation to make real decisions. The IRS discusses governance practices for charities in its governance and related topics guidance for section 501(c)(3) organizations. For a new organization, that usually means resisting the temptation to fill every seat with relatives, business partners, or the founder’s inner circle.

Set up your board records with future reporting in mind from day one. Store signed bylaws, incorporator actions, conflict disclosures, meeting minutes, and policy approvals in one place. An integrated platform helps here because the legal file, board actions, and financial history stay connected. That reduces the common startup problem where the accountant has one version of events, the secretary has another, and the grant report needs a third.

State fundraising rules are easy to miss

Federal tax exemption does not replace state charity registration rules.

Many states require a separate registration before a nonprofit solicits donations, and the details vary by where donors are located and how the organization asks for support. The National Council of Nonprofits explains these state-level obligations in its charitable solicitation registration resource.

That creates a practical risk early on. A nonprofit can be properly incorporated and still be out of step with state law if it starts taking online gifts, sending appeal emails, or launching a public campaign before the right registrations are handled.

Here’s where founders usually get tripped up:

| Issue | What founders assume | What actually matters |

|---|---|---|

| State incorporation | “We formed the nonprofit, so we can fundraise” | Incorporation and fundraising registration are often separate |

| IRS filing | “Federal status covers everything” | Federal tax-exempt status does not replace state charity rules |

| Early donation asks | “We’re small, so this won’t apply yet” | Public solicitation can trigger registration duties early |

If you need a practical reference while sorting local filings, this guide to nonprofit incorporation state by state is useful to keep open alongside your formation checklist.

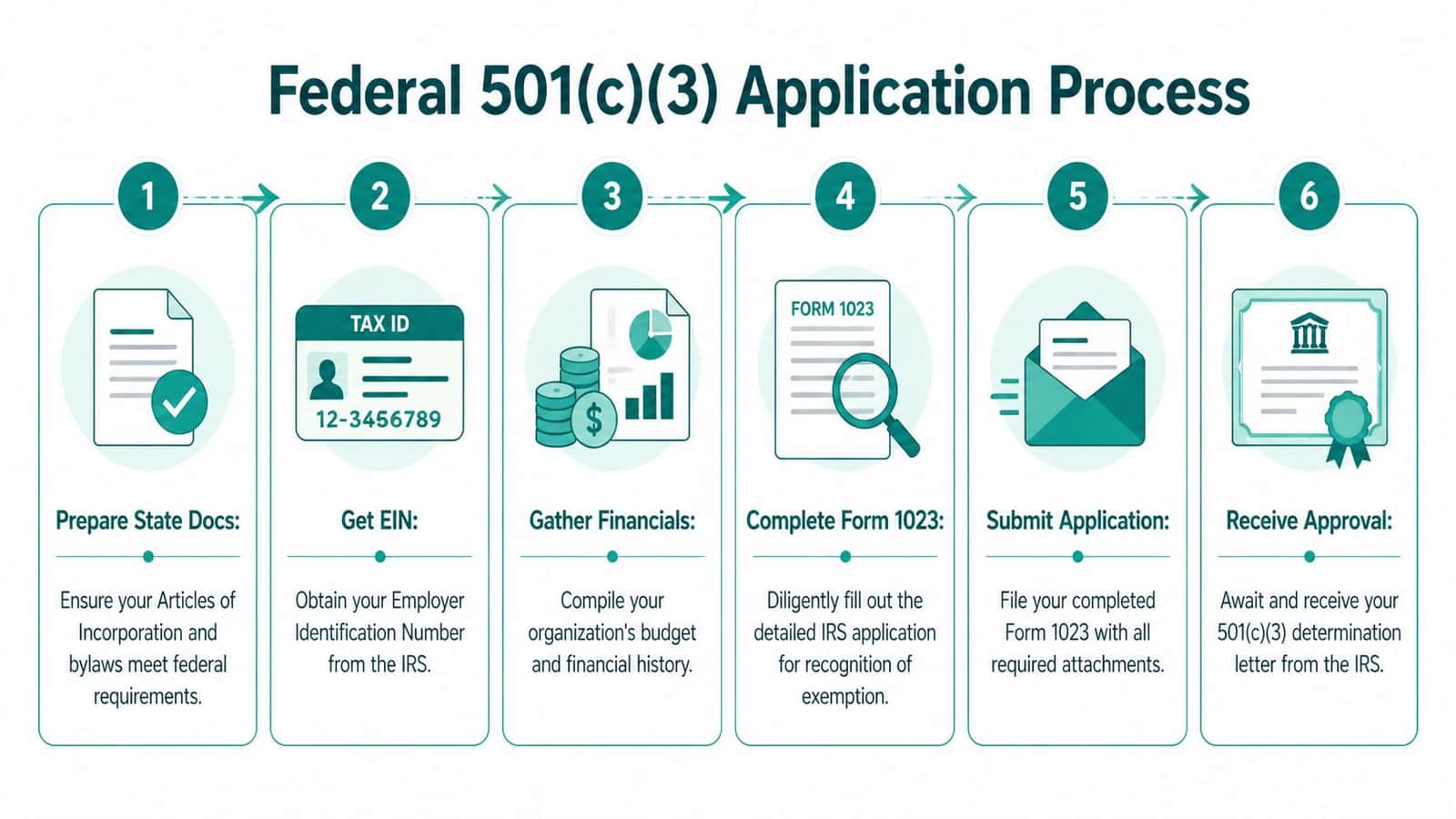

The Main Event Filing for Federal 501(c)(3) Status

A board approves the mission, opens a bank account, and starts planning programs. Then the federal application lands on someone’s desk and the mood changes fast. The form is not impossible, but it does punish vague plans, loose records, and governance decisions that were never documented properly.

Treat this filing like the first real test of how your organization will operate. Groups that set up their documents, budgets, and records in one place usually move through it with less confusion. Groups that piece everything together from email threads, scattered PDFs, and old spreadsheets often create their own delays.

Start with the EIN

Before filing for federal exemption, get an Employer Identification Number. You will need it for the IRS application, banking, payroll, and other basic setup work.

This step is simple. The discipline around it matters more than the form itself.

Store the EIN confirmation with your organizing documents, signed bylaws, conflict of interest policy, board minutes, and any resolutions the board has adopted. That habit pays off later when the IRS asks for consistency across your legal documents, financial plan, and program description.

Choose between Form 1023 and Form 1023-EZ carefully

The right filing path depends on the organization’s structure, projected finances, and eligibility for the shorter form. As noted earlier, timing matters if you want exemption recognized back to incorporation.

Do not choose Form 1023-EZ just because it looks faster. The shorter form can be appropriate for a simple organization that clearly qualifies. It is a poor fit when the nonprofit has related-party transactions, unusual programming, complicated revenue plans, or facts that need explanation.

The full Form 1023 takes more work, but that work often helps a board make better early decisions. It forces founders to define programs, tighten governance, and match the budget to actual plans. That is not busywork. It is operational planning in legal form.

What the IRS is looking for

First-time founders often focus on completion. The IRS is looking for coherence.

Your application needs to show that the mission, activities, governance, and finances all fit together. If the narrative says you will run youth tutoring, the budget should show program supplies, staffing or volunteer support, and a realistic way to fund that work. If the board includes insiders or family members, the governance documents should show how conflicts are disclosed and managed.

A strong filing answers four practical questions:

| IRS question | What your application should show |

|---|---|

| Why do you exist | The purpose fits 501(c)(3) charitable rules |

| What will you do | The activities are specific, regular, and mission-driven |

| Who makes decisions | The board can exercise independent judgment and manage conflicts |

| How will money be used | Revenue and expenses support programs, not private benefit |

That last point deserves more attention than many boards give it.

The mistakes that trigger delays

Weak applications usually do not fail because of one dramatic error. They stall because the filing reads like an idea that has not been turned into an organization yet.

The most common trouble spots are familiar:

- Purpose statements that are too broad: A mission that tries to cover every public good often says less, not more.

- Program descriptions that stay abstract: The IRS wants to know what you will do, for whom, how often, and by what method.

- Board relationships that raise independence questions: Family-heavy boards and insider arrangements need careful documentation and control policies.

- Financial projections that do not match the narrative: If the budget and the program plan tell different stories, reviewers notice.

I have seen new nonprofits spend days polishing values language and only an hour on the budget. That choice usually comes back to bite them. Financial projections are where the IRS tests whether your plans can operate practically.

Why the financial section deserves more attention

The budget is not a side attachment. It is one of the clearest signals that the board understands how the organization will function.

Use the financial section to show where revenue will come from, what programs it will support, and how administrative and fundraising costs will be tracked. If you plan to rely on grants, say which kinds. If individual giving is part of the model, show a reasonable path for that. If you expect earned revenue, explain how it relates to the mission.

This is also the moment to set up systems that will still work a year from now. An integrated platform from day one can save a new nonprofit from re-creating records later for Form 990 preparation, grant reporting, donor acknowledgments, and board review. If donations, restrictions, expenses, and program activity live in separate places, the application may get filed, but the reporting headaches start immediately after.

If you want a practical reference while assembling the packet, use this Form 1023 checklist for attachments, narratives, and governance documents.

Get another set of eyes before you file

A careful review before submission is money well spent.

That does not require hiring a large law firm in every case. It does mean someone with exempt organization experience should read the application as a package, not just proofread individual answers.

Ask the reviewer to check four things:

- Whether the Articles include the required exempt purpose and dissolution language.

- Whether the activity narrative proves charitable operation, not just charitable intent.

- Whether the budget supports the story told elsewhere in the application.

- Whether conflicts, compensation, and insider relationships are disclosed and governed properly.

A good review often costs less than a delayed filing, a long IRS follow-up, or months spent rebuilding records that should have been organized from the start.

You're Approved Now Comes Lifelong Compliance

Three months after approval, a board member asks a simple question. How much grant money is still available, what donor restrictions are outstanding, and who is tracking the filing deadlines? New nonprofits rarely get in trouble because the mission is weak. They get in trouble because the legal setup was never turned into a working system.

The determination letter starts a different kind of work. From that point on, the organization has to prove, year after year, that its money, decisions, and programs match its stated purpose. Groups that treat approval as the end of the process usually end up rebuilding records under pressure, often right before a filing, an audit request, or a grant report.

Form 990 should shape how you keep records all year

Most tax-exempt organizations file some version of Form 990 each year, depending on their size and receipts. That filing is public. Donors, funders, watchdog groups, and prospective board members read it.

That changes how a smart founder sets up operations.

If accounting lives in one tool, donor records in another, grant files in email, and board approvals in scattered folders, Form 990 prep turns into a reconstruction project. If those records are connected from day one, the annual return becomes a review process instead of a scramble.

Good records protect the mission and the people leading it

Clean documentation does more than satisfy the IRS. It protects board members, staff, and volunteers when questions come up about spending, approvals, or donor intent.

Keep records that answer the practical questions a real reviewer will ask:

- Board minutes that show who approved major decisions and when

- Donation records that clearly note restrictions and acknowledgments

- Grant files that connect awards, budgets, reporting deadlines, and approved uses

- Program records that show services delivered match the organization’s stated purpose

- Expense support that explains what was spent, for whom, and under which fund or program

I have seen young nonprofits lose weeks chasing basic answers that should have been available in five minutes. The issue was not bad intent. The issue was scattered systems.

Restricted funds expose weak systems fast

Restricted money is where compliance problems become operational problems.

A scholarship fund, a capital campaign gift, or a program-specific grant cannot be treated as general cash just because it sits in the same bank account. If the organization cannot track what came in, what was spent, and what remains restricted, leadership starts making decisions on guesses. That is how boards overcommit funds, miss reporting terms, or give donors conflicting answers.

The trade-off is straightforward:

| Approach | What it feels like early on | What it creates later |

|---|---|---|

| Spreadsheet tracking | Cheap and familiar | Version control problems and weak audit trails |

| Basic small-business bookkeeping | Manageable with very simple activity | Limited visibility into restrictions, programs, and grant reporting |

| Fund-based records in an integrated system | More setup discipline at the start | Clearer board reports, cleaner grant tracking, and faster Form 990 prep |

This is why future operations matter during legal setup. The chart of accounts, donation categories, approval workflows, and document storage choices you make in year one determine whether compliance stays manageable in year three.

Put deadlines and reviews where the whole board can see them

Compliance fails when too much knowledge sits with one treasurer, one founder, or one outside bookkeeper.

Build a short annual calendar that includes IRS filing deadlines, state renewals, board review dates, grant report due dates, acknowledgment deadlines, and document retention checks. Keep it visible. A new treasurer should be able to step in, read it, and understand the organization’s responsibilities without a long handoff meeting.

For a practical template, use this Form 990 checklist for nonprofits and board filing prep.

The goal is not more paperwork. The goal is fewer surprises, cleaner reporting, and a system that keeps working when staff changes, the board turns over, or a funder asks harder questions.

Making It All Manageable A Modern Toolkit for New Nonprofits

Most directors I know are wary of software promises, and they should be. Too many products solve one narrow problem, then leave your staff exporting data, retyping gifts, and patching together reports before every board meeting.

That matters more during startup than vendors admit. The tools you choose in year one shape how hard compliance feels in years two and three.

The setup problem is really an operations problem

A federal filing asks for purpose, governance, and financial clarity. Those aren’t abstract legal concepts. They’re operating realities.

The verified data from Wolters Kluwer’s tax-exempt filing overview says roughly 20-30% of 501(c)(3) applications are denied or withdrawn. It identifies leading causes such as incomplete purpose clauses, failure to prove exclusively charitable activities, and poor financial documentation. The same source notes that many new nonprofits risk their $600 application fee and months of delay, while Form 1023-EZ sees a 70% auto-approval rate for eligible organizations, even though up to 40% of applicants struggle with the eligibility worksheet itself.

The legal lesson is obvious. The operating lesson is just as important. If you can’t document what you do and how you handle money, your filing gets weaker.

What works better than a pile of separate tools

A practical toolkit for a new nonprofit should reduce duplicate entry and make board-ready reporting easier. It should also fit the way nonprofits work, which usually means finance, fundraising, volunteers, events, and communications overlap every week.

That’s where all-in-one systems can earn their keep, especially for smaller teams.

For example, many organizations start with a mix like QuickBooks for accounting, Bloomerang for donor records, SignUpGenius for volunteers, Mailchimp for email, and Eventbrite for events. Those are all credible tools. QuickBooks is familiar. Bloomerang is donor-friendly. Mailchimp is widely known. Eventbrite handles ticketing well.

The gap isn’t that these tools are bad. The gap is that they weren’t built as one operational record for a nonprofit. That creates friction when your treasurer wants restricted fund detail, your development director wants campaign results, and your board wants one version of the truth.

The capabilities that matter early

For a young organization, I’d focus less on flashy features and more on these outcomes:

- Fund accounting that respects restrictions: Not classes pasted onto business accounting, but actual fund-level reporting.

- Donor management connected to finance: Gifts, receipts, pledges, and balances should line up without hand reconciliation.

- Volunteer records in the same operating system: This matters for schools, churches, and service groups that run on people as much as money.

- Built-in communication tools: Email, text, and giving pages are easier to manage when they aren’t detached from donor history.

- Board-friendly reporting: If reports require heroic cleanup every month, the system is costing more than it appears.

A strong modern platform can also help fiscal sponsors and multi-program organizations. Those groups need cleaner project separation, clearer reporting, and fewer user access headaches than generic small-business tools usually provide.

If you’re comparing approaches, this guide to nonprofit accounting software is a practical place to evaluate what true nonprofit finance support looks like.

Where AI can help and where it should not

AI is becoming part of nonprofit operations, but directors should stay clear-eyed about it. It can help summarize data, surface anomalies, draft first-pass communications, and answer routine internal questions.

It should not replace board judgment, finance review, or legal advice.

Used well, an AI assistant can save time for leaders who don’t want to chase reports or dig through menus. Used poorly, it becomes another layer between you and the facts. The right standard is simple. If the tool helps you see your own data more clearly, good. If it hides the logic, be cautious.

Choose tools that shorten the distance between the transaction and the board report.

The best startup systems also make room for growth. A church may need donor records, designated giving, volunteers, and event communication. A school may need grants, restricted programs, and parent engagement. A fiscal sponsor may need project-level reporting and clean internal controls. The legal path to nonprofit status is similar, but the operational burden looks different in each case.

That’s why the smartest founders think beyond approval. They choose structures, records, and tools that still make sense once donations increase, grants arrive, and annual filings become routine.

If you're building a nonprofit and want fewer moving parts from day one, Alignmint is worth a serious look. We built it for nonprofit leaders who need true fund accounting, donor management, volunteers, events, marketing, team communication, and AI help in one place, with plan-based user allowances (1 on Free, up to 10 on Plus, up to 25 on Pro, and unlimited on Enterprise). For organizations raising under $100K, the free tier gives you a practical way to start with better habits before compliance gets hard.

Frequently Asked Questions

Ready to try Alignmint with your nonprofit?

Start free — set up donor tools, giving pages, and Minty AI. Upgrade when you need accounting.