Unlock Your Nonprofit's Statement of Financial Position

For related tools, see Alignmint features.

Quick Answer: Unlock Your Nonprofit's Statement of Financial Position

A nonprofit statement of financial position is the nonprofit version of a balance sheet. It shows assets, liabilities, and net assets on a specific date so leaders can explain cash, debt, restricted balances, and what is actually available for mission work.

You’re probably looking at a board packet right now, or you will be soon, wondering whether the numbers tell a clear story. Not just whether they add up, but whether you can explain them with confidence when someone asks, “Can we afford this?” or “Is that grant money available?”

That’s where the statement of financial position helps. It gives you a clean snapshot of what your nonprofit owns, what it owes, and what’s left for mission work, so you can walk into board meetings, grant reviews, and donor conversations with a steadier voice.

Gain Confidence in Your Financial Story

The hardest part of nonprofit finance isn’t always the math. It’s the quiet pressure of feeling like you should already know what every line means.

A lot of executive directors carry that pressure alone. You may have a bookkeeper, an outside accountant, or a volunteer treasurer, but when the board starts asking questions, the answers still land on your desk.

That’s especially true in smaller nonprofits, churches, schools, and fiscal sponsor settings, where formal finance training often isn’t part of the job. As Blackbaud’s overview of the statement of financial position notes, practical guidance often misses the actual needs of leaders who don’t have dedicated finance staff.

You don’t need to become an accountant. You need to know what decisions the report supports.

The statement of financial position matters because it answers very practical questions.

- Can you hire now: Or is your cash tied up in restricted funds.

- Can you reassure the board: That short-term bills can be covered without scrambling.

- Can you report to funders cleanly: Without guessing which balances belong to which program.

- Can you spot trouble early: Before a year-end review turns into a painful surprise.

If your annual reporting process still feels heavy, it helps to see how the financial story fits into the broader message you share with supporters. Our annual report template for nonprofits is useful for that bigger picture.

Why this report feels harder than it should

Many resources explain definitions. Fewer explain what to do with the report on an ordinary Tuesday when payroll is due, a grant reimbursement is late, and your board chair wants a financial update by noon.

That’s why it helps to read the statement of financial position like a leadership tool, not an accounting test. Once you know what each section is telling you, the report becomes less intimidating and far more useful.

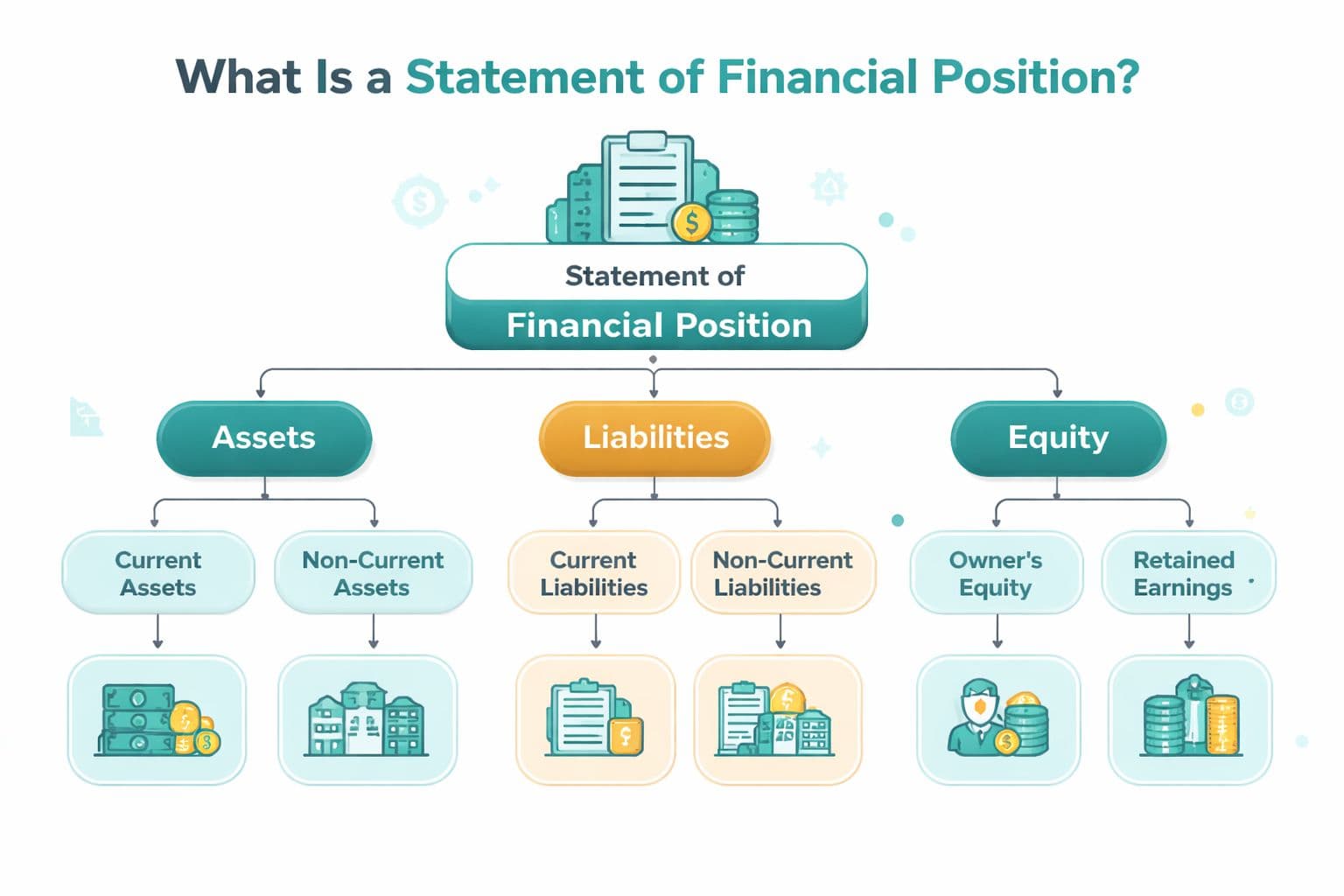

What Is a Statement of Financial Position

At its simplest, a statement of financial position is a snapshot of your organization’s finances on one specific date. It shows what you own, what you owe, and what remains after those obligations are considered.

For nonprofits, the basic equation is Assets = Liabilities + Net Assets, as explained by Nonprofit Accounting Basics. In the same example, total assets of $30,000 and total liabilities of $5,000 leave $25,000 in net worth or net assets.

If you want a short reference version of the definition, this statement of financial position glossary entry is a good bookmark.

Start with what you own

Assets are the resources your nonprofit controls. Think cash in the bank, money owed to you, supplies, equipment, and other items that support your mission.

A simple example makes this easier to picture. In one example from Nonprofit Accounting Basics, assets include cash $10,000, accounts receivable $5,000, supplies $3,000, equipment $10,000, and intangibles $2,000, for total assets of $30,000.

Then look at what you owe

Liabilities are your obligations. These can include bills to vendors, short-term loans, payroll-related amounts, or longer-term debt.

In that same example, liabilities include accounts payable $2,000 and short-term loans $3,000, for total liabilities of $5,000. Once those are subtracted from assets, the remaining value belongs in net assets.

Practical rule: If a board member asks whether you’re “doing okay,” they’re usually asking about cash, debt, and what’s actually available to spend.

Why the snapshot matters

A statement of financial position is different from a report that covers a whole month or year. It captures one moment in time.

That matters because some dates can look stronger or weaker than others. A reimbursement might not have arrived yet. A grant payment may be recorded, but restricted. A large bill may be due next week, even if today’s cash balance looks calm.

Here’s the simplest way to read it:

- Assets tell you what resources are on hand.

- Liabilities tell you what claims already exist against those resources.

- Net assets tell you what remains, subject to nonprofit restrictions that matter a great deal.

Once you see those three pieces clearly, the report stops looking like a wall of numbers and starts answering real operational questions.

The Key to Nonprofit Reporting Net Assets

Nonprofit reporting parts ways with for-profit language in this context. In a nonprofit, the equity section is replaced by net assets, and those net assets must be shown in categories with donor restrictions and without donor restrictions, as explained by AccountingCoach.

That distinction isn’t cosmetic. It tells you whether money is available for general operations or committed to a specific purpose.

If you want a clean definition to share with staff or board members, this net assets glossary entry is a helpful reference.

What unrestricted really means

Net assets without donor restrictions are the resources you can generally use for operations, staffing, rent, utilities, and other current needs. This is the part of the report many directors want to find first, because it speaks to breathing room.

But even here, you still need judgment. Money may be technically unrestricted and still needed for payroll next month, a pending insurance payment, or a board-designated reserve.

What restricted means in daily life

Net assets with donor restrictions are not available for whatever need feels urgent today. If a donor or grant agreement limits the use of funds, those amounts must stay identified separately.

That’s why this section matters so much during stressful periods. You may see cash in the bank, but not all cash is spendable for general operations.

Restricted money can sit in your account and still be off limits for payroll, rent, or a surprise repair.

A youth program grant is a simple example. If funds were given for that program, those resources belong under donor-restricted net assets until used according to the restriction. If the money hasn’t been spent on that purpose yet, you can’t treat it as free operating cash, even if the bank balance looks healthy.

For leaders juggling grants and compliance, it’s worth reviewing a practical guide to charity bookkeeping compliance alongside your internal reports. It can help clarify where reporting discipline protects both mission and trust.

Where leaders often get tripped up

The confusion usually isn’t about the words. It’s about the decision attached to them.

Common trouble spots include:

- Seeing cash and assuming flexibility: Cash can include restricted grant funds that can’t support general overhead.

- Mixing board intent with donor intent: A board reserve and a donor restriction are not the same thing.

- Treating grant balances as earned freedom: If the grant terms still apply, the restriction still matters.

- Reporting restricted funds as available liquidity: That can mislead your board and create compliance problems.

This is one reason the statement of financial position becomes a governance tool, not just a finance report. It helps leadership avoid accidental missteps before they become audit findings or awkward funder conversations.

The question behind the question

When someone asks, “How much do we have,” the better question is, “How much do we have that we can use for this purpose right now?”

That’s the question net assets answer. Once you start reading this section that way, your board conversations become sharper, your grant reporting gets cleaner, and your budget choices become more grounded.

How the SOFP Differs from a Balance Sheet or Form 990

People often use statement of financial position and balance sheet as if they mean exactly the same thing. In many conversations, they do. But for nonprofit leaders, the terminology helps signal an important difference in how your organization is structured and reported.

The bigger point is this. Your board may say “balance sheet,” your accountant may say “statement of financial position,” and your tax preparer may focus on Form 990. Those are related, but they’re not interchangeable.

Nonprofit SOFP vs for-profit balance sheet

| Component | Nonprofit Statement of Financial Position | For-Profit Balance Sheet |

|---|---|---|

| Ownership section | Uses net assets | Uses equity or stockholders’ equity |

| Restriction focus | Separates amounts with and without donor restrictions | Focuses on owner value, retained earnings, and capital |

| Decision lens | Spendability, compliance, and mission support | Profit, ownership value, and returns |

| Board conversation | “What can we use and what is restricted?” | “What do owners hold after liabilities?” |

If your team also reviews operating results, it helps to understand how profit-focused reporting differs from nonprofit reporting. This piece on mastering profit and loss gives a useful contrast.

Why Form 990 is different

Your Form 990 is an annual filing. Your statement of financial position is one of the underlying reports that helps you prepare it.

That’s why classification matters so much. The statement of financial position must separate assets and liabilities into current and non-current, and that structure affects liquidity review and cash-flow planning, as described by IAS Plus on IAS 1. For nonprofits, that distinction also shows whether restricted grant funding is available for near-term program needs or tied up longer term.

Here’s the practical version:

- Current assets are resources likely to turn into cash within the near term.

- Non-current assets are longer-term items like property or equipment.

- Current liabilities are obligations due in the near term.

- Non-current liabilities are obligations extending further out.

That classification affects more than formatting. It helps you answer questions like these:

- Can we meet short-term obligations

- Is this grant funding available now or later

- Are we mistaking long-term strength for short-term cash health

A nonprofit can look stable on paper and still feel tight on cash if too much value sits in long-term or restricted categories.

The link between your reports

Think of the statement of financial position as the report that organizes your standing on a given date. Form 990 then pulls from that organized data, along with your other financial records, into a compliance document for the IRS.

That’s why sloppy classification creates downstream pain. When current and non-current items are mixed together, or restricted balances aren’t clearly identified, year-end prep gets slower and more stressful.

If you want a broader orientation to that filing process, this Form 990 guide for new nonprofits is a useful next read.

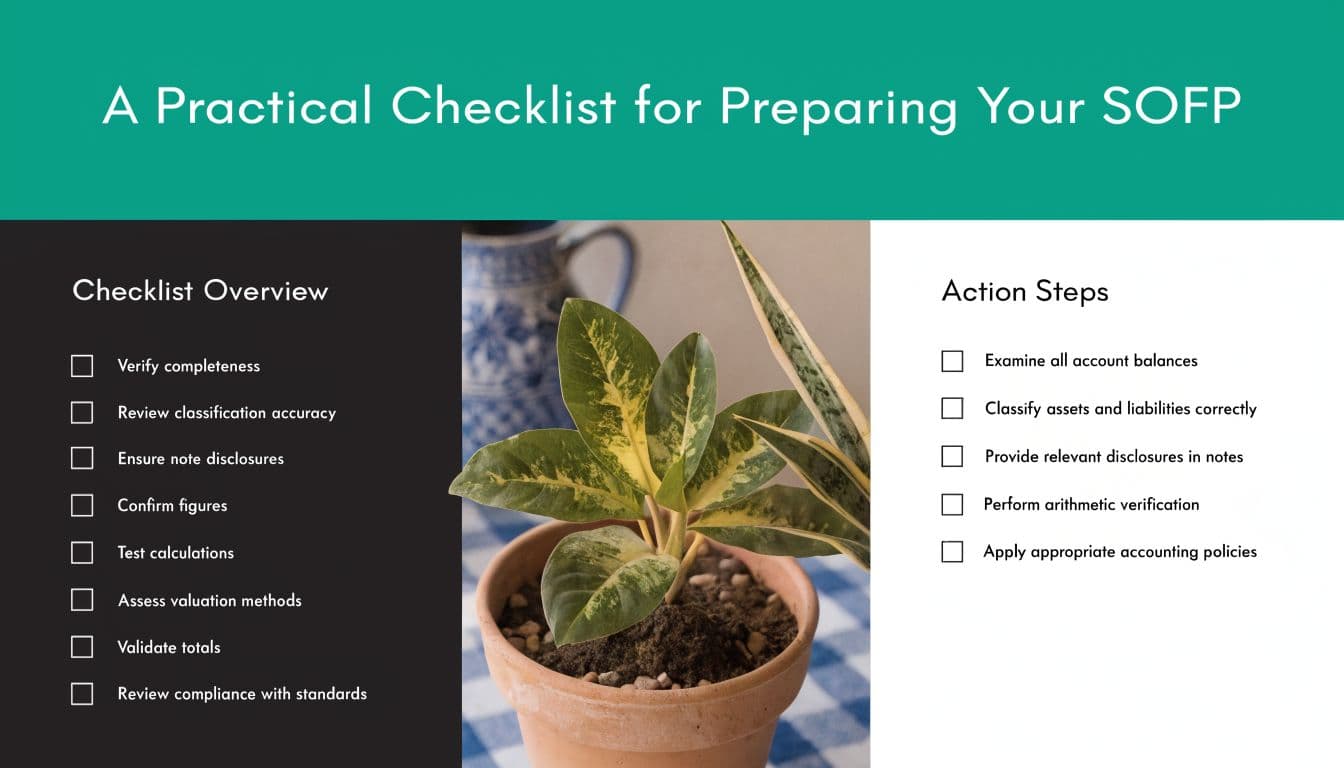

A Practical Checklist for Preparing Your SOFP

Before a board meeting, I’d treat the statement of financial position like a sanity check. You’re not trying to impress anyone with accounting language. You’re making sure the report supports the decisions in front of you.

One of the fastest checks is the liquidity ratio, which is current assets divided by current liabilities. As RCGT explains in its discussion of key financial indicators, a ratio over 1.0 suggests an organization can cover short-term obligations. Their example shows $125,000 in current assets and $90,000 in current liabilities, producing a liquidity ratio of 1.39.

Your pre-meeting review list

- Check the report date: A strong report from the wrong date can still lead you to the wrong conclusion.

- Review cash first: Then ask how much of that cash is restricted versus available for general operations.

- Scan receivables carefully: Pledges and reimbursements matter, but they aren’t the same as cash in hand.

- Separate current from non-current items: This affects how realistic your liquidity picture is.

- Confirm restricted balances: Make sure grant and donor limitations still match the underlying records.

- Look at short-term obligations: Payables, loan payments, and other near-term commitments shape your real flexibility.

- Calculate liquidity ratio: If it’s above 1.0, that’s a sign you can cover short-term obligations, using the RCGT framework above.

Common mistakes that create confusion

Some errors show up again and again in smaller nonprofits.

One is treating a board-designated amount as if it were donor-restricted. Another is counting a pledged gift as available cash before timing is clear. A third is assuming a grant award is fully spendable without checking its purpose and timing conditions.

Boardroom check: If a line item would take more than two sentences to explain, it probably needs cleanup before the meeting.

For leaders reviewing their bookkeeping process more broadly, this article on strategic investment in bookkeeping offers a practical outside perspective.

A simple file-prep habit that helps

Keep one clean list of your core balance sheet accounts and how each should be classified. If your chart of accounts is messy, your statement of financial position usually will be too.

This nonprofit chart of accounts template can help you tighten that foundation. It’s especially useful if you’ve inherited years of inconsistent naming or reporting.

If you’re comparing software, it’s fair to say QuickBooks is familiar and strong for many organizations. But nonprofits often end up building workarounds with classes and manual tracking. A true fund accounting approach can reduce that cleanup because restricted funds, grants, and programs are tracked in the accounting structure itself rather than patched on later.

From Financial Reports to Financial Confidence

When you understand your statement of financial position, financial conversations stop feeling like a trap. You can answer the board with clarity, speak to donors with integrity, and make staffing or program decisions with a steadier hand.

That confidence matters because nonprofit leadership is already demanding. You’re managing mission, people, deadlines, and funding uncertainty. Your financial reports should support that work, not add another layer of fog.

The right system won’t remove every hard decision. But it can make the numbers easier to trust, easier to explain, and easier to act on. That’s especially helpful when your accounting, donor records, volunteers, events, and communications all affect the same day-to-day picture.

If you want that kind of clarity without stitching together separate tools, take a look at Alignmint. We built it as an all-in-one platform for nonprofits that need true fund accounting, donor management, volunteer tracking, events, marketing, team communication, and AI help in one place. For smaller organizations, there’s a free tier for nonprofits under $100K, plan-based user allowances (1 on Free, up to 10 on Plus, up to 25 on Pro, and unlimited on Enterprise), and Minty AI to answer questions from your real data without extra exports.

Ready to try Alignmint with your nonprofit?

Start free — set up donor tools, giving pages, and Minty AI. Upgrade when you need accounting.