For related tools, see Alignmint features.

OMB A-133 Explained: A Nonprofit's Guide to the Single Audit

Quick Answer: OMB A-133 Explained: A Nonprofit's Guide to the Single Audit

OMB A-133 is the old name for the federal Single Audit required when your organization expends enough federal awards in a fiscal year. The trigger is federal expenditures, not just receiving a grant. Prepare with clean SEFA support, restricted-fund tracking, documented approvals, and records that tie grant terms to ledger entries.

Federal money can change your year. It can also drop a phrase into your grant agreement that makes your stomach tighten: OMB A-133. If you're staring at that term and wondering whether you've just signed up for a bureaucratic headache, the short answer is this: it's manageable when your records are clean and your team knows the rules.

I've been through enough audits to tell you this plainly. A Single Audit is not a mystery test. It's a practical check on whether your organization tracks federal funds, follows grant rules, and can prove what happened. If you get the basics right early, you can face it calmly.

That Confusing Term in Your New Grant Agreement

You win a federal grant. Your program team is relieved, your board is pleased, and then somebody forwards the agreement with one line highlighted: compliance with OMB A-133.

That's usually when the questions start. Is this a special audit. Does it apply right now. Do you need a consultant. Did anyone on your team already miss something important.

Most executive directors don't need more jargon. You need a straight answer. OMB A-133 is the old name many people still use for what is now called the Single Audit. If you want a plain-language definition, this Single Audit glossary entry is a useful starting point.

Why the term still shows up

Grant language often lags behind practice. Lawyers, agencies, and pass-through entities may still use the older term even though the formal framework changed years ago.

That doesn't mean you're behind. It means you're seeing old shorthand that never fully disappeared.

Practical rule: When you see OMB A-133 in a grant document, read it as a signal to check your federal spending, your records, and your audit readiness.

The core issue isn't the label. The core issue is whether your operation is organized enough to show where the money went, what restrictions applied, and who approved the spending.

If that sounds less like accounting and more like organizational discipline, that's because it is. In my experience, federal compliance problems usually expose operational problems first. Weak approval paths. Disconnected records. Grant terms stored in email. Finance and development working from different assumptions.

That's why this topic matters even before an audit is required. It tells you whether your house is in order.

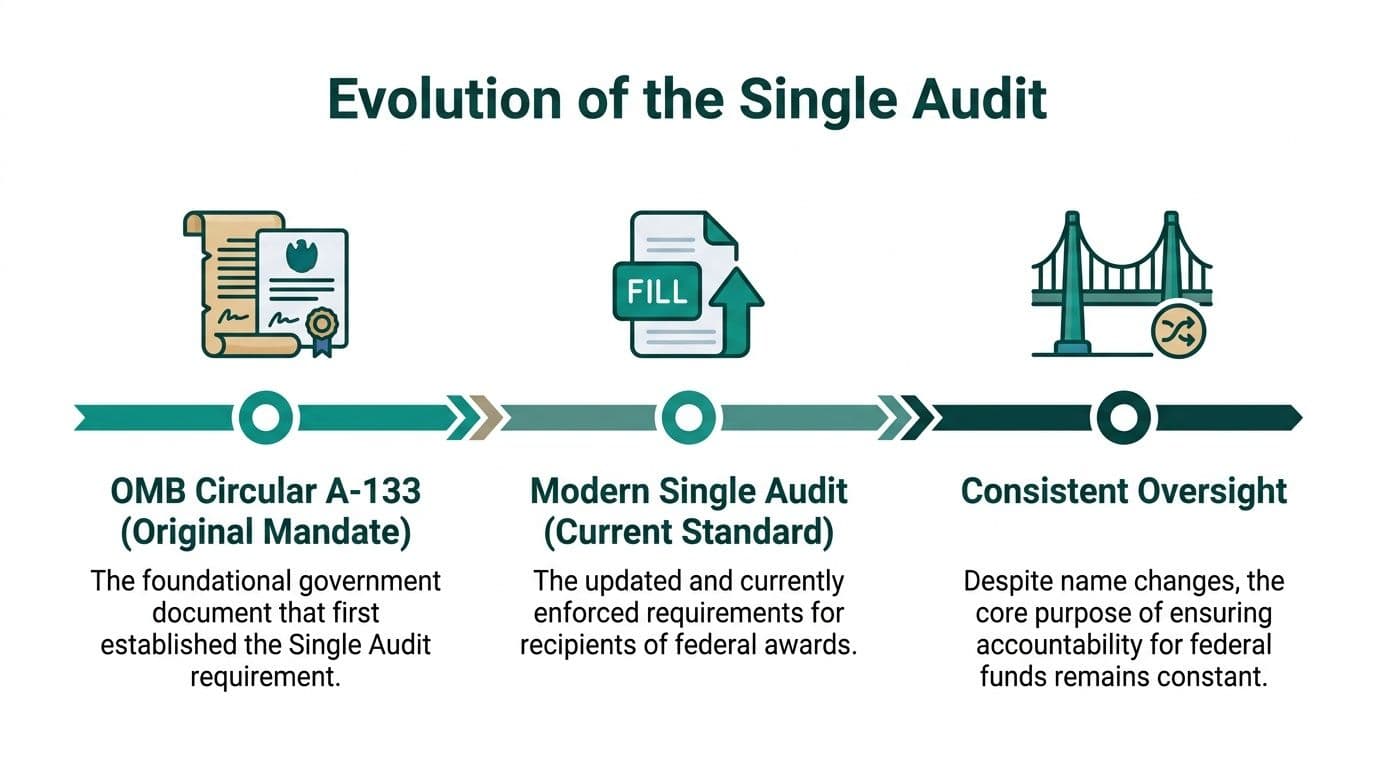

From OMB A 133 to the Modern Single Audit

Let's clear up the naming first. OMB A-133 is the old street name. Single Audit is the name on today's road sign.

The requirement began with the Single Audit Act of 1984 and OMB Circular A-133. That framework was later updated by the Uniform Guidance in 2014, which also raised the audit threshold over time from $500,000 to current levels and consolidated multiple audit reports into one thorough review, as summarized in the OMB A-133 Compliance Supplement background.

What changed and what didn't

The name changed. The organizing idea did not.

Federal agencies needed a consistent way to review organizations spending federal awards. Before that, separate reviews could pile up around the same money. The Single Audit model created one coordinated review instead of a patchwork.

Here's the simple version:

| Then | Now |

|---|---|

| OMB Circular A-133 | Uniform Guidance |

| "A-133 audit" | Single Audit |

| Multiple agency-specific audit burden | One comprehensive review |

That matters because many nonprofit leaders hear the old term and assume it refers to some retired process. It doesn't. The label is dated, but the compliance duty is very much alive.

Why executive directors should care

This history isn't trivia. It helps you speak clearly with auditors, grant managers, and board members.

If someone on your team says, "Do we need an A-133," the better question is, "Do our federal expenditures trigger a Single Audit under current rules?" That wording is cleaner, and it keeps everyone focused on the actual requirement.

The safest approach is to treat old terminology as a translation issue, not a legal loophole.

I also think the 2014 shift carried an important message for nonprofit leaders. Federal oversight moved toward a more unified review because fragmented reporting wastes time and creates confusion. Your own internal setup should follow that same logic. When accounting, donor records, volunteer activity, program spending, and team communication all live in separate places, audit prep turns into a scavenger hunt.

That's especially true for churches, schools, and fiscal sponsors. Those organizations often manage restricted activity across several programs at once. If your records are split between QuickBooks, spreadsheets, inboxes, and a donor database that doesn't talk to finance, the audit becomes harder than it needs to be.

The point of the modern Single Audit isn't to punish you. It's to verify that your organization can account for public money in one coherent system.

Do You Actually Need a Single Audit

Many ask the wrong question. They ask, "We got federal money. Are we automatically in audit territory?"

No. Many small nonprofits mistakenly believe the Single Audit applies to them regardless of size, but the current threshold is strictly for those with $750,000 or more in annual federal expenditures. Organizations below this are not required to undergo a Single Audit but must still maintain proper internal controls, as noted in this explanation of what triggers an A-133 audit.

The decision comes down to one core test

Ask this first: How much federal money did your organization expend during the fiscal year?

Not pledged. Not awarded. Not promised. Expended.

If your federal expenditures are below the current threshold, you may not need a Single Audit. That does not mean you can relax your controls. You still need clear records, disciplined approvals, and support for every federal transaction.

A few practical checks

Use this short screen before you panic:

- Check the spending, not just the award letter: A big grant award can sound alarming, but the audit trigger hinges on what your organization expended in the fiscal year.

- Confirm whether funds are federal awards: Some money reaches you through a state or another nonprofit. You still need to know whether the original source is federal.

- Separate audit rules from state rules: Your state may have its own financial review thresholds. This guide to nonprofit audit requirements by state can help you sort state-level obligations from federal ones.

- Get a financial readiness check early: If you're close to the line, a financial readiness review can show whether your records are prepared for formal scrutiny.

If you're under the threshold, that's not a free pass. It's a chance to get your systems right before the stakes rise.

There's one more wrinkle worth knowing. The threshold is changing for certain future periods, but you should apply the rule based on the fiscal year that governs your audit. Don't mix today's requirement with tomorrow's threshold and confuse your board.

For a busy executive director, the takeaway is simple. Don't guess. Calculate federal expenditures carefully, document the conclusion, and revisit it before year-end if spending accelerates.

What a Single Audit Actually Involves

If you do cross the line, the audit itself is less mysterious than people think. It has two sides. One examines your financial statements. The other examines whether you followed the compliance rules tied to federal awards.

The official guidance matters here. The OMB A-133 Compliance Supplement is the official guide auditors use. It states that any non-Federal entity expending $1,000,000 or more, effective for fiscal years ending on or after September 30, 2025, must undergo both a financial statement audit and a program compliance audit, according to the University of Washington single audit summary.

The financial side

This part feels familiar if you've had a regular audit. Auditors look at whether your financial statements are presented properly and whether your accounting records support them.

They'll care about basics that reveal discipline:

- Cash and reconciliations: Are your balances tied out and current.

- Revenue and expense classification: Did you record activity in the right place.

- Restricted and unrestricted treatment: Did you separate what was limited from what was available.

- Internal control evidence: Can your team show who approved, posted, and reviewed transactions.

For organizations handling grants, donor restrictions, and multiple programs, clean fund accounting matters here. If you need a refresher on the mechanics, this guide to fund accounting for nonprofits is worth reading.

The compliance side

At this stage, federal funding gets specific. Auditors test whether you followed the grant rules, maintained required documentation, and spent money on allowable purposes.

Think of the compliance audit as a match test. The auditor compares your records against grant terms, federal requirements, and your own control procedures.

A Single Audit doesn't just ask whether you spent the money. It asks whether you spent it the right way, documented it properly, and can prove both.

Why the SEFA matters so much

The Schedule of Expenditures of Federal Awards, or SEFA, is the master list that anchors the process. It summarizes federal funds expended by program.

If your SEFA is shaky, everything after it gets harder. If it's clean, the audit has a reliable map.

That's why I tell executive directors to stop treating the SEFA as a year-end fire drill. It should be the natural result of disciplined recordkeeping across the year. When your accounting records, grant files, and supporting documents agree with each other, the SEFA becomes a report. When they don't, it becomes a reconstruction project.

Common Audit Problems and How to Prevent Them

Audit trouble usually starts long before the auditor arrives. It starts when a nonprofit normalizes workarounds.

A spreadsheet tracks one grant. QuickBooks classes track another. Development keeps donor letters in a shared drive. Program staff approve spending by email. Then everyone hopes finance can tie it together later.

That approach is fragile. It might limp along in a quiet year, but federal funding exposes every weak joint.

The failures I see most often

The repeat problems are boring, which is exactly why they're dangerous.

- Restriction trails break: A donor or grant restriction exists, but nobody can trace it cleanly from source document to ledger entry.

- Documentation lives in too many places: Invoices sit in email, payroll support lives in a folder, and approvals are remembered rather than recorded.

- One person does too much: The same staff member receives money, posts entries, reconciles accounts, and answers auditor questions.

- Generic software is stretched past its design: QuickBooks is familiar and strong for many small organizations, but classes are still a workaround when you need true fund accounting.

The restricted-funds issue deserves special attention. Auditors routinely test whether donor restrictions are clearly documented and can be traced from the original donor agreement through to the general ledger. This requires a system that tracks funds across multiple dimensions, not just a spreadsheet, and reconciles regularly to catch issues early, as described in this article on restricted funds tracking and audit readiness.

Better systems prevent ordinary mistakes

I'm not interested in software hype. I am interested in avoiding avoidable findings.

Here's the practical distinction:

| Patchwork approach | Purpose-built approach |

|---|---|

| Restrictions tracked in notes or classes | Restrictions tracked directly in the accounting structure |

| Donor records and finance records drift apart | Gift intent and accounting treatment stay connected |

| Audit support assembled manually | Support is easier to trace and review |

| Team access limited by extra seat costs in many tools | More people can participate in controls and review |

If you're comparing tools, be fair. QuickBooks is a solid general accounting product. Salesforce is powerful for CRM. Bloomerang is well known in donor management. Planning Center is familiar in churches. Blackbaud has deep history in the sector. The issue isn't that these tools are weak. The issue is that many nonprofits end up stitching together separate systems and then asking staff to bridge the gaps by hand.

Your audit result often reflects your daily operating model. Messy systems create messy answers.

If your organization handles school funds, church programs, volunteer activity, fiscal sponsorship, or restricted gifts, the line between "accounting issue" and "operations issue" disappears quickly. That's why clean team communication matters as much as chart-of-accounts design. Finance can't document what program staff never recorded.

For a deeper look at the accounting side of this, this resource on tracking restricted funds covers the discipline auditors expect.

A Practical Checklist to Prepare for Your Audit

Good audit prep is not glamorous. It's orderly. That's better.

The biggest mistake I see is waiting until fieldwork is scheduled. By then, your team is tired, files are scattered, and everyone treats the auditor request list like a crisis. You want the opposite. You want a repeatable routine.

The core standard is simple. To pass an audit, organizations must prepare a Schedule of Expenditures of Federal Awards, or SEFA, which summarizes all federal funds expended. The absence of a valid SEFA or unsupported expense documentation like invoices and payroll records can directly cause an audit failure, according to this explanation of the Single Audit formerly known as the A-133 audit.

Your working checklist

Keep this practical. Assign an owner and a due date to each item.

-

Pull every grant agreement into one folder. You need the award document, amendments, reporting terms, and any correspondence that changed spending rules.

-

Write down your approval path. Who can approve expenses. Who enters transactions. Who reconciles the bank account. Who reviews reports.

-

Build the SEFA from your books, not from memory. If finance has to rebuild federal spending from emails and spreadsheets, your controls are already weak.

-

Attach support to the transaction. Invoices, receipts, payroll records, and allocation support should be easy to retrieve.

-

Review restricted activity before year-end. Don't wait for the auditor to discover that spending and restriction terms don't match.

-

Test one grant from start to finish. Pick a federal award and trace it from agreement to expense support to ledger to report.

The executive director's role

You do not need to become a technical accountant. You do need to insist on discipline.

Ask these questions in your finance meeting:

- Can we produce support for any federal expense without searching email?

- Can we explain our approval process in writing?

- Can we show restricted balances clearly?

- Can our team trace one grant through the ledger and reports?

Those are leadership questions, not bookkeeping questions.

The best audit prep starts when records are created, not when requests arrive.

If your organization also handles sensitive financial data for sponsored projects or donor-advised activity, it helps to understand broader control frameworks too. This checklist on SOC 2 compliance for CEFs is useful context for thinking about documentation, access, and evidence discipline across systems.

One last point. Don't let the checklist stop at finance. Development, program leads, school administrators, church staff, volunteer coordinators, and grant managers all create records that auditors may follow later. If the whole team understands that, audit prep stops feeling like a finance department burden and starts working like an organizational habit.

The Right System Turns Compliance into Confidence

An OMB A-133 question is rarely just an audit question. It's a health check on how your nonprofit runs.

If your team tracks grants in one place, donor intent in another, volunteer activity somewhere else, and marketing responses in a separate tool, you're asking people to hold the organization together by memory. That's risky. It also wastes leadership time.

A better setup gives you one operating picture. Accounting, CRM, volunteers, events, marketing, online giving pages, and team communication should support each other instead of fighting each other. That matters for ordinary management. It matters even more when federal dollars enter the mix.

What confidence looks like in practice

Confidence is not bravado. It's being able to answer ordinary questions quickly.

Can you see restricted balances clearly. Can your development and finance teams agree on gift intent. Can your church or school team separate federal funds from other activity. Can a fiscal sponsor track each sponsored project without a spreadsheet maze. Can staff pull support without calling three departments.

That's the standard I'd hold.

Modern nonprofit leaders should also expect more from their systems than static reporting. AI tools can help surface missing documents, identify unusual coding patterns, and answer questions about your own data. Marketing tools should already sit close to donor records. Volunteer records should not be detached from program delivery. And unlimited user access matters because good controls depend on shared visibility, not bottlenecks.

If you're evaluating platforms, be practical. Look for true fund accounting, not class tracking dressed up as fund accounting. Look for donor management that connects to finance. Look for online giving pages, volunteer management, and a built-in marketing suite so your team isn't chasing exports. If your organization is small, pricing matters too. A free tier for nonprofits under $100K can help you build good habits before growth makes cleanup expensive.

For a closer look at what purpose-built nonprofit accounting should include, review these fund accounting features.

If you want fewer spreadsheets, cleaner audit prep, and one place to manage accounting, donors, volunteers, events, marketing, and team visibility, take a look at Alignmint. We built it for nonprofit leaders who need true fund accounting, unrestricted and restricted clarity, Minty AI help with real operational questions, unlimited users without per-seat fees, and a free tier for nonprofits under $100K.

Ready to try Alignmint with your nonprofit?

Start free — set up donor tools, giving pages, and Minty AI. Upgrade when you need accounting.