For related tools, see Alignmint features.

Chargebacks and Disputes: A Nonprofit's Survival Guide

Quick Answer: Chargebacks and Disputes: A Nonprofit's Survival Guide

Nonprofit chargebacks and disputes are forced card reversals that often start from confusion, not fraud. Prevent them with clear statement names, recurring terms, fast receipts, and easy support. When one arrives, match evidence to the reason code, preserve the original gift in your books, and post a proper reversal in true fund accounting.

A donor gives on Friday night. By Monday morning, your finance lead sees a dispute notice, your development director is confused, and nobody knows whether the gift was restricted, recurring, or already acknowledged.

That's why chargebacks and disputes can't sit in a payment silo. In a nonprofit, they touch donor trust, fund accounting, receipting, reporting, and the daily work of protecting resources meant for the mission.

What Are Chargebacks and Why Do Donors File Them

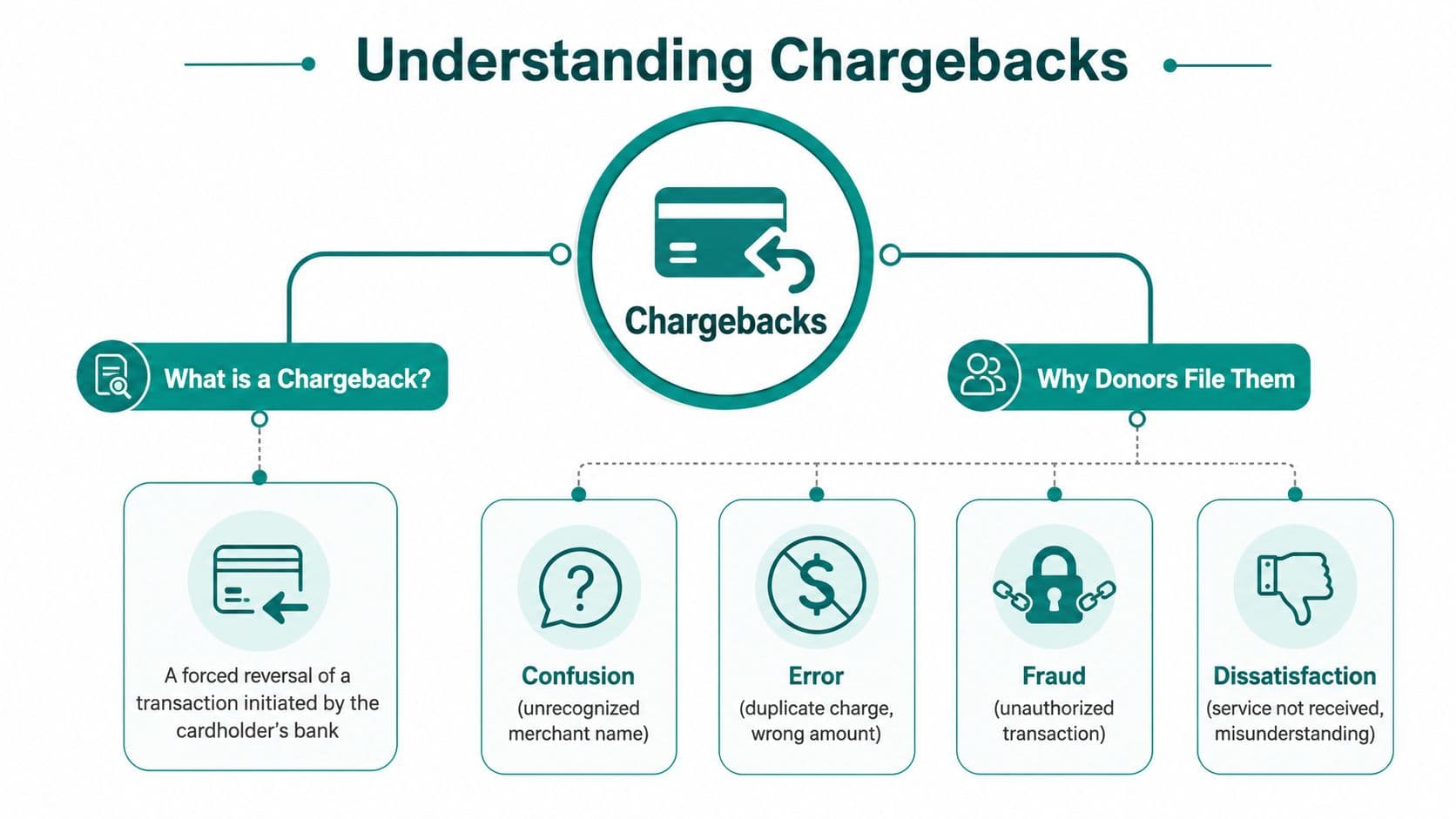

A chargeback is a forced reversal of a card transaction started through the donor's bank. A dispute can begin earlier, as the donor questions a charge or asks the bank to investigate it.

For nonprofit leaders, that distinction matters. A donor who is confused today can become a formal chargeback tomorrow if your team is hard to reach, your receipts are unclear, or the bank statement name doesn't match what the donor remembers.

The four reasons I see most often

Most chargebacks are not dramatic fraud cases. They are ordinary breakdowns in recognition, memory, or service.

- Confusion about the charge: The donor doesn't recognize the name on the bank statement, especially after an event, campaign, or fiscal sponsorship arrangement.

- A payment error: The donor believes they were charged twice, charged the wrong amount, or charged after trying to cancel a recurring gift.

- Actual unauthorized use: Someone used the donor's card without permission.

- Dissatisfaction or misunderstanding: The donor expected one thing and believes they received something else, or they never contacted your team before calling the bank.

The most important shift is this. Many disputes are not really about criminal fraud. They're about convenience and communication.

According to Verifi's chargeback triangle research, 55% of chargebacks are now consumer preference driven, not fraud. In plain language, the donor found it easier to call the bank than to ask you for help.

Practical rule: If it's easier to dispute than to contact your office, you'll keep seeing preventable chargebacks.

Why nonprofits get caught off guard

Nonprofits often assume goodwill protects them. It doesn't. A donor may fully support your mission and still dispute a charge because they forgot a recurring gift, didn't recognize your descriptor, or had a family member use the card.

Donor stewardship matters as much as payment handling. If your receipts are prompt, your recurring terms are plain, and your support contact is visible, many of these issues never become formal disputes. Good stewardship of donors is often your first defense.

What a dispute usually signals

A dispute is often a symptom, not the root problem. It usually points to one of these gaps:

- Recognition failed. Your statement name, event brand, or campaign name didn't match what the donor remembered.

- Expectations weren't clear. The donor missed the recurring frequency, refund terms, or event delivery details.

- Response was too slow. The donor couldn't get a quick answer from your team, so the bank became the shortcut.

A chargeback notice is rarely just a payment problem. It's often a delayed message that the donor journey broke somewhere earlier.

If you lead a church, school, or sponsored project, this gets even messier. Donations, fees, registrations, and recurring support can all look similar on a statement. When your systems are disconnected, your team spends precious time reconstructing the story after the fact.

The True Cost of Disputes to Your Mission

The donation amount is only the first loss. The bigger damage comes from staff time, outside fees, and the distraction from work your team wants to do.

Mastercard reports that each chargeback imposes an average total cost of $128 on a U.S. merchant. That total includes $82 in internal operational costs and $46 in third-party fees, and that's before the lost donation value.

The cost your board can't see on the processor screen

The processor may show one disputed transaction. Your team experiences something else.

- Finance time: Someone has to locate records, confirm coding, and determine whether the gift touched a restricted fund.

- Development time: Someone has to review donor emails, recurring history, receipts, and past interactions.

- Leadership time: Someone decides whether to fight, refund, or accept the loss and move on.

That time doesn't come from nowhere. It comes from grant reporting, volunteer coordination, donor care, event planning, and all the ordinary work already crowding your week.

Why small organizations feel this most

A larger organization can spread this burden across departments. A smaller nonprofit usually can't. The same person may manage donor records, bookkeeping, acknowledgments, and online giving pages.

When that person stops to handle a dispute, the mission work waits. So does the monthly close.

The real cost of a chargeback is often the interruption. It pulls your leanest people into reactive work at exactly the wrong time.

The strategic risk

Chargebacks and disputes also create a pattern risk. If they stack up, payment partners may view your organization as harder to support. That can complicate online giving, especially for nonprofits that depend on recurring donations, event registrations, tuition payments, or church contributions.

This is why prevention deserves budget attention. It isn't administrative fussiness. It protects cash flow, donor relationships, and your ability to keep receiving gifts online without added friction.

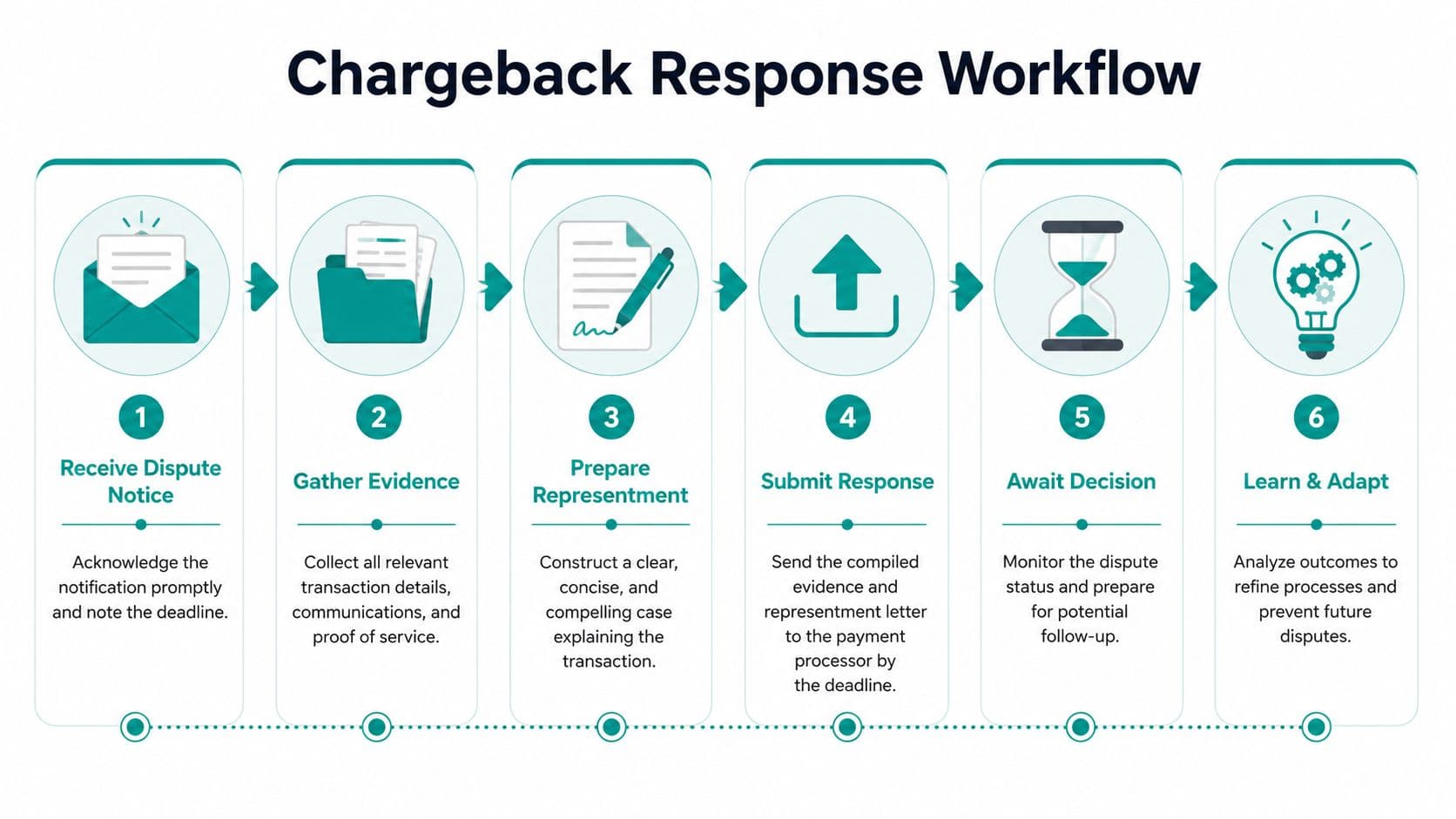

Your Step-by-Step Guide to Responding

When a dispute lands, speed matters more than emotion. You need a disciplined response, a clear file, and one owner for the process.

The formal process is longer than most leaders expect. The chargeback dispute workflow typically spans 60 to 75 days, and if you lose the initial dispute and appeal, arbitration fees can reach hundreds of dollars. That's why the first evidence packet matters so much.

Start with triage, not outrage

The first question is simple. Was the charge valid?

If the payment was unauthorized or your organization made a clear error, accepting the chargeback may be the right move. Fighting a valid claim wastes staff time and weakens credibility.

If the charge appears valid, gather your facts before anyone writes a response. Pull everything into one folder or case file, including records from your payment system, donor CRM, event tool, and accounting notes. If your team needs a practical reference for workflows and status handling, review your payment management documentation.

The seven steps in plain English

Here's the process most merchants move through:

- The donor files the chargeback through the issuing bank.

- The issuing bank reviews the claim and usually grants a provisional credit if the dispute fits an accepted category.

- The acquiring bank notifies the merchant.

- The merchant decides whether to accept the chargeback or submit representment with evidence.

- The acquiring bank sends the evidence package to the issuer.

- The issuer decides whether to reverse or uphold the chargeback.

- Arbitration may follow if the merchant appeals and the card network steps in.

That sequence sounds technical, but your work is straightforward. Build the clearest possible narrative with documents that match the dispute reason.

Don't send every record you have. Send the records that directly answer the bank's reason code.

What compelling evidence looks like for nonprofits

Product merchants often rely on shipping proof. Nonprofits usually need a different file.

For a donation, your strongest evidence may include the receipt email, the donor's giving history, recurring authorization, and the campaign page shown at the time of the gift. For an event, you may need registration records, attendance logs, confirmation emails, and delivery details for digital access.

If you want a broader outside reference on assembling evidence and rebuttals, these chargeback fighting strategies are useful reading.

Nonprofit Evidence Checklist for Chargeback Representment

| Evidence Type | What to Include |

|---|---|

| Donation receipt | Confirmation email, receipt number, date, amount, donor name, and wording shown to the donor |

| Recurring authorization | Signup screen, recurring terms, frequency selection, checkbox consent, and confirmation message |

| CRM history | Prior gifts, notes, donor communications, refund requests, and account updates |

| Payment record | Transaction ID, timestamp, processor response, card authorization details, and billing data on file |

| Campaign or appeal record | Donation page copy, event registration details, sponsorship language, or fund designation shown at checkout |

| Service or event delivery proof | Attendance log, ticket confirmation, digital access record, livestream registration, or campaign participation record |

| Communications file | Emails with the donor, support replies, refund discussions, and any acknowledgment of the charge |

A practical response workflow

I've found the most reliable workflow looks like this:

- Assign one owner: Finance and development both contribute, but one person controls deadlines and final submission.

- Match the evidence to the claim: "Did not recognize," "did not receive," and "unauthorized" each need different proof.

- Write a brief cover summary: Keep it factual. Explain what the transaction was, what the donor agreed to, and why the charge was valid.

- Submit before the deadline: A late response usually loses by default.

- Record the lesson: If the donor was confused, fix the recurring language, statement descriptor, or acknowledgment flow.

When not to fight

Some disputes should be accepted quickly. If the documentation is weak, the amount is small, or the transaction involved an internal mistake, move on and fix the process.

That decision is not weakness. It's stewardship. Save your team's energy for the cases you can document clearly and defend properly.

How to Prevent Disputes Before They Happen

Prevention starts with one principle. Make it easier to get help from you than from the bank.

Bank of America notes that up to 50% of disputes could be resolved before they become chargebacks if nonprofits implement real-time donor self-service portals with clear terms and easy refund processes. That should get every executive director's attention.

Fix the moments that create confusion

Most preventable chargebacks begin long before the dispute is filed. They begin on the donation page, in the receipt email, or on the bank statement.

Here are the prevention moves that matter most:

- Use a recognizable statement name: If your legal entity, school name, campaign brand, and church name all differ, donors may not connect them.

- Make recurring gifts unmistakable: State the amount, frequency, and next charge date in plain language.

- Show refund and contact options clearly: A donor who can reach a real person quickly is less likely to call the bank first.

- Send immediate confirmation: The receipt should remind the donor what they gave to, when, and how to contact you.

A lot of organizations still bury this information. That's expensive.

Your donation page does more than collect gifts

A giving page is not just a form. It is a risk control tool.

If the page is vague, donors fill in the blanks later with their own assumptions. If the page is clear, it prevents confusion at the source. These nonprofit donation page best practices are worth reviewing with both development and finance in the room.

A clean giving page protects revenue twice. It helps the donor say yes, and it reduces the chance they'll question the charge later.

The role of security and trust

Some disputes are driven by real unauthorized activity, so security still matters. If your nonprofit depends on online forms, event registrations, and donor accounts, basic application security is part of donor trust. For leaders who want a plain-English view of the risk, this overview of SaaS pentesting is a useful starting point.

What works better than a tougher policy

Many organizations respond to chargebacks by tightening language and adding friction. That usually backfires. Donors don't need a more intimidating checkout experience. They need clarity and a fast path to support.

The better approach is simple:

- Put your contact information where donors can see it.

- State recurring terms before payment, not after.

- Let donors manage their own giving when possible.

- Resolve refund requests quickly and politely.

- Review dispute patterns by campaign, event, or payment type.

Disconnected systems prove to be a real handicap. If your donor data, event data, communications, and accounting records live in different places, your team can't spot patterns early. The result is more confusion, slower responses, and more avoidable disputes.

Accounting for Chargebacks in Your Nonprofit Books

Many general guides often miss the full picture. A chargeback is not just a returned payment. It is an accounting event that can affect fund balances, receivables, revenue, and reporting.

Under ASC 958 guidance for restricted contributions, a restricted contribution is recorded as revenue when the pledge is made, not only when cash arrives. If that gift later turns into a chargeback, you need a careful reversal to stay compliant.

Why deleting the original donation is the wrong move

I still see organizations solve this by deleting the gift from the donor record or voiding the original entry in generic bookkeeping software. That creates a false history.

You need the original transaction to remain visible. It happened. The better approach is to record the reversal correctly so your audit trail, donor history, and financial statements still tell the truth.

That's especially important if the gift touched a restricted fund, a grant-supported program, a church campaign, or a school tuition-related activity. The accounting has to reflect what happened, when it happened, and which fund was affected.

What to review before you post the reversal

Before your team posts anything, confirm these items:

- Fund designation: Was the original gift unrestricted, temporarily restricted, or part of a donor-designated purpose?

- Pledge versus cash timing: Was revenue already recognized before the cash settled?

- Receipting status: Did the donor already receive an acknowledgment or tax receipt?

- Reporting impact: Will the reversal affect a grant report, campaign total, or board report already shared?

If you want a broader refresher on the underlying bookkeeping discipline, this guide to mastering nonprofit accounting is a good companion read.

A practical bookkeeping approach

At minimum, your records should preserve three things:

| What to preserve | Why it matters |

|---|---|

| Original gift entry | Maintains donor and audit history |

| Reversal entry | Shows the financial correction clearly |

| Fund impact | Keeps restricted and unrestricted balances accurate |

Your settlement and reconciliation process also matters. If your team can't see what settled, what was reversed, and what hit the bank, month-end close turns into detective work. A clear donation settlement report helps finance staff tie the dispute activity back to real deposits and reversals.

The accounting goal isn't to erase a bad transaction. It's to document it correctly so your books remain trustworthy.

Why true fund accounting matters here

QuickBooks can be a useful general ledger, and many nonprofits know it well. Bloomerang, DonorPerfect, and Kindful are strong in donor relationship work. Blackbaud has long experience with larger organizations. But most combinations of separate tools leave chargeback handling fragmented.

That fragmentation becomes a problem when a disputed gift touches restrictions, pledges, multiple programs, or fiscal sponsorship reporting. You don't just need categories. You need true fund accounting that can reverse activity without breaking donor history or misstating balances.

How Alignmint Reduces Your Chargeback Risk

Chargebacks and disputes get worse when your records are split across separate tools. One system holds the donation, another holds the donor, another holds event details, and accounting sits somewhere else. That gap is where confusion grows.

We built Alignmint to close that gap. Your accounting, donor management, volunteers, events, marketing suite, online giving pages, and team communication live in one place. That means a disputed transaction is easier to trace from the original gift, to the receipt, to the donor profile, to the fund entry.

For nonprofits under $100K, our free tier gives smaller teams a practical starting point without adding seat costs. For growing organizations, unlimited users help finance, development, church office staff, school administrators, and volunteer leaders work from the same record. Minty AI helps your team surface transaction context quickly, and our true fund accounting handles restricted funds in a way class-based tools don't.

If you're comparing options, it's fair to say that tools like QuickBooks, Bloomerang, DonorPerfect, Salesforce, and Blackbaud each do certain jobs well. The gap is that they often require more handoffs, more reconciliation, and more room for chargeback confusion. Our donation pages connect directly to the rest of your nonprofit operations, which makes prevention and response much easier.

If you want fewer surprises, cleaner books, and a better donor experience, take a look at Alignmint. We built it for nonprofit leaders who need true fund accounting, donor management, volunteers, events, marketing, and AI help in one place, without per-seat fees and without a maze of disconnected systems.

Ready to try Alignmint with your nonprofit?

Start free — set up donor tools, giving pages, and Minty AI. Upgrade when you need accounting.