For related tools, see AlignMint features.

Reimbursement Expense: A Guide for Nonprofit Leaders

Quick Answer: Reimbursement Expense: A Guide for Nonprofit Leaders

A reimbursement expense is a mission-related cost someone paid personally and your nonprofit later paid back. Treat it as a financial control: collect the receipt, confirm the business purpose, assign the right fund, approve it separately, and keep the payment trail attached.

You probably have a stack of receipts on someone's desk, a few reimbursement emails buried in Outlook, and a quiet concern that one late form could become a payroll problem. That's common in nonprofits, especially when one person is juggling finance, programs, donor reporting, and HR at the same time.

A clear reimbursement expense process fixes more than paperwork. It protects restricted funds, keeps your books clean, and helps your Form 990 reflect the programs your mission is funding.

Your Guide to Managing Reimbursement Expenses

A reimbursement expense process should give you confidence, not another monthly scramble. When it's handled well, your staff gets paid back promptly, your records stay audit-ready, and your finance team stops chasing missing details.

Most nonprofits start with good intentions and weak systems. Someone buys supplies, forwards a receipt, and expects finance to sort out the coding later. That approach is expensive. The total cost to process a single reimbursement can range from $14 to $50, with cycle times averaging 15-20 days, largely because people are fixing missing receipts and unclear approvals by hand, according to APQC expense reimbursement benchmarks.

The simple way to think about it

An accountable plan works like lending a trusted friend money for a specific errand. They tell you what they bought, hand you the receipt, and return any extra cash. If any of those pieces are missing, it stops being a clean repayment and starts looking like compensation.

That distinction matters more than many directors realize. Reimbursement policy isn't just an HR document. It affects payroll treatment, grant reporting, functional expenses, and board confidence.

Practical rule: If your team can't explain who spent the money, why they spent it, and which fund should bear the cost, the reimbursement isn't ready for approval.

What a workable process should give you

You need a system that answers a few questions quickly:

- Business purpose: Why was this expense necessary for your mission or operations?

- Documentation: Is there a receipt, mileage log, or other support attached?

- Timing: Was it submitted within your policy window?

- Fund coding: Should it hit general operations, a grant, a school program, or a church ministry budget?

- Reporting impact: Will it flow correctly into your functional expense reporting?

If you also work across countries or partner organizations, it helps to compare how expense rules differ elsewhere. For readers who want that broader context, this guide to financial management for Australian businesses offers a useful outside perspective on documenting business expenses.

What Counts as a Reimbursement Expense

A reimbursement expense is money your organization pays back to someone who spent personal funds for a legitimate business purpose. The clean version is straightforward. The person incurred the cost for your nonprofit, documented it properly, and didn't keep any excess amount.

The IRS framework behind that is the accountable plan. In plain terms, three things need to be true. The expense must have a business connection, the person must substantiate it on time, and any extra advance or overpayment must be returned.

A four-part mental model that helps

Most reimbursement confusion clears up when you sort requests across two questions. Who incurred the expense, and are you paying actual costs or using an allowance approach?

| Person | Actual documented expense | Per diem or allowance |

|---|---|---|

| Employee | Usually the cleanest path when receipts or logs support the business purpose | Can work if your policy defines when it applies and how it's documented |

| Volunteer | Often appropriate for approved out-of-pocket mission costs | Needs extra care, since loose flat payments can drift into taxable or unsupported territory |

That table won't answer every edge case, but it does show where risk rises. Actual documented expenses are easier to defend. Flat payments need tighter policy language and stronger review.

Employee versus volunteer requests

Employees usually submit reimbursements through a formal expense process. Volunteers often submit them informally, which is where trouble starts. A volunteer who buys event supplies with personal funds still needs the same basic discipline. Date, amount, purpose, and support.

For employees, wage law can also come into play. The Fair Labor Standards Act requires employers to reimburse nonexempt employees for job-related expenses if those costs would reduce their pay below the federal minimum wage, as explained in this FLSA reimbursement overview.

What actual expense means in practice

Actual expense reimbursement means the person is repaid for what they really spent, not an estimate. That's why finance teams ask for itemized receipts, mileage logs, conference agendas, or notes showing who attended a meal and why it was necessary.

If you need a clean starting point for gathering that information, this expense reimbursement form example is a practical reference.

If the support is vague, the accounting will be vague too. That's how good intentions turn into bad reporting.

A strong reimbursement expense policy reduces that ambiguity before the purchase happens, not after.

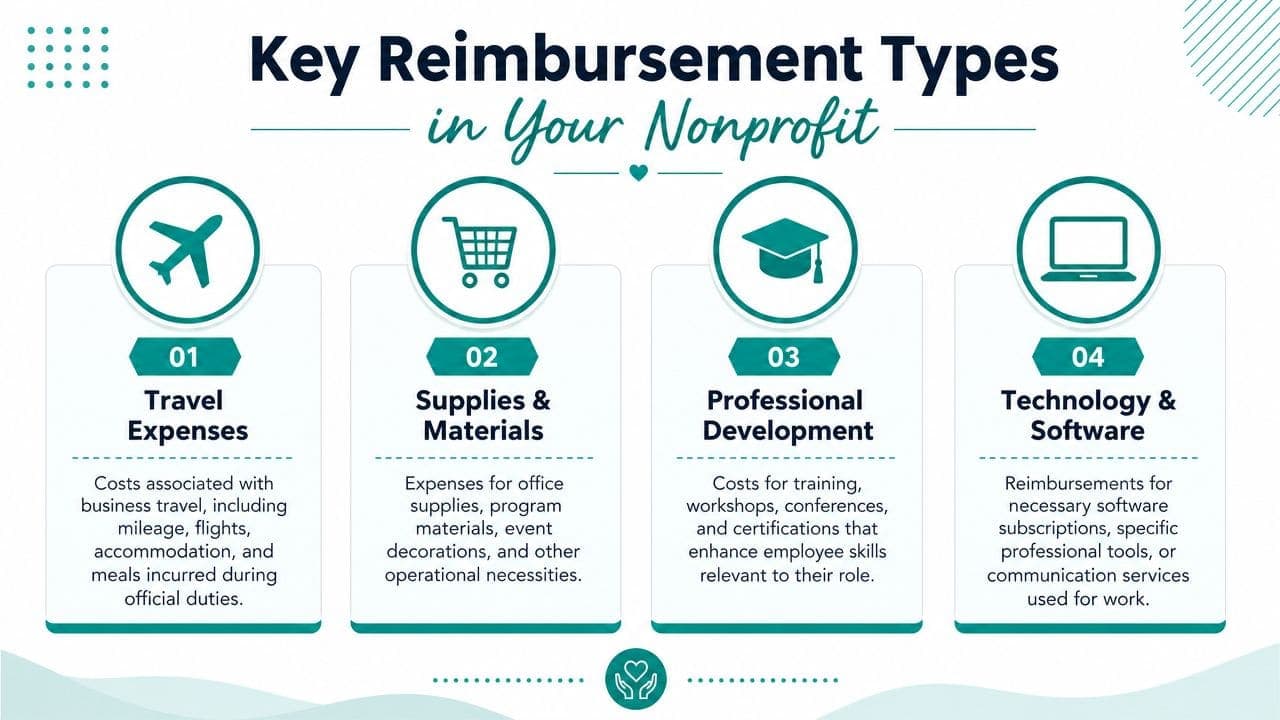

Key Reimbursement Types in Your Nonprofit

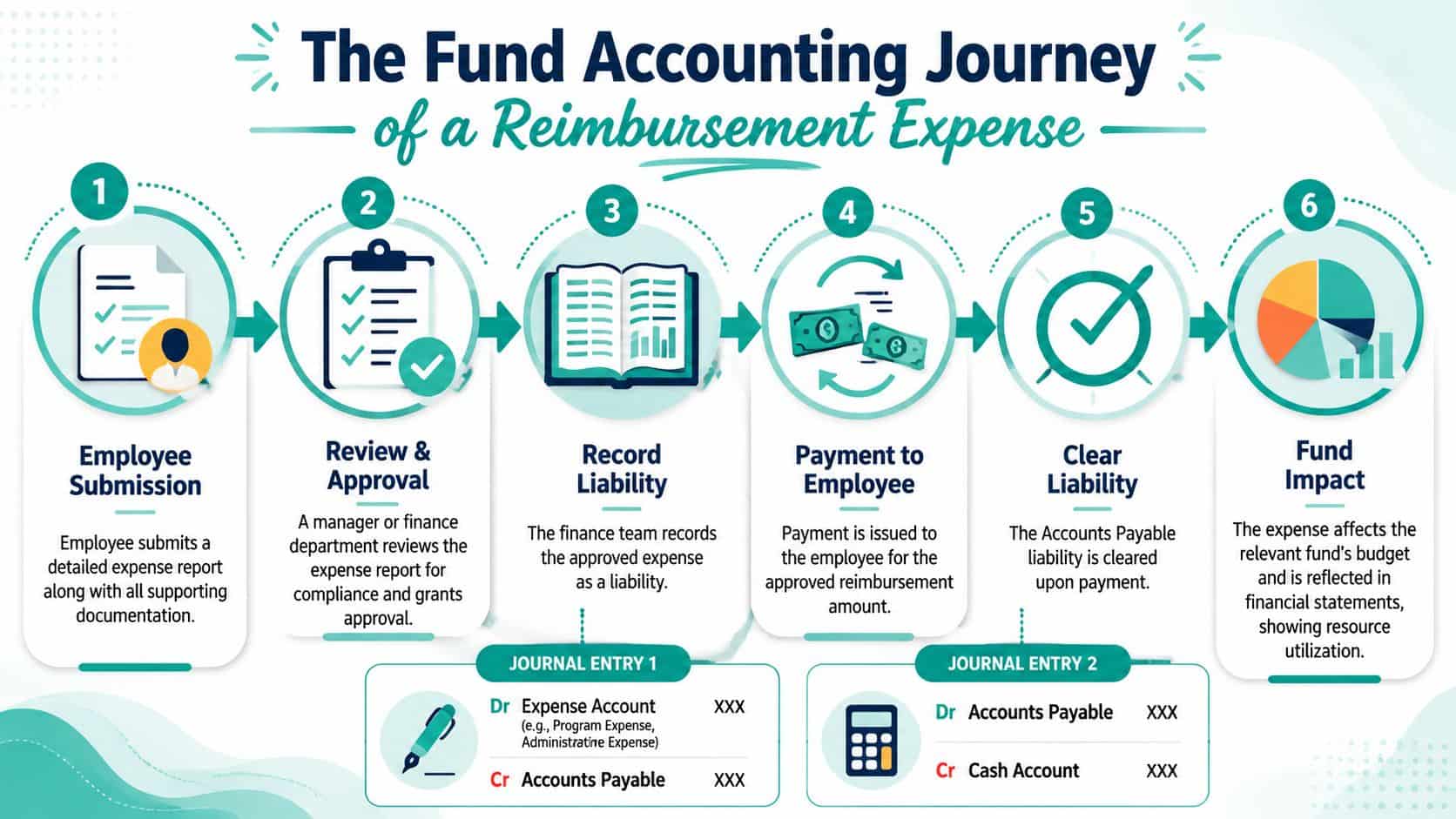

The easiest reimbursement expense to record is one paid from unrestricted operating funds. A staff member buys program supplies, the manager approves the request, and finance records the cost in the proper expense account. Then the reimbursement is paid and the liability is cleared.

The harder version is common in nonprofits. The same purchase might belong to a grant, a school activity fund, a church outreach budget, or a fiscally sponsored project. If you code it loosely on the way in, you'll spend far more time cleaning it up later.

Start with the journal entry

For a standard approved reimbursement, many teams record it in two steps:

-

Approve and record the obligation

- Debit the relevant expense account

- Credit accounts payable or an employee reimbursement liability

-

Issue payment

- Debit accounts payable

- Credit cash

That structure matters because it creates a clear audit trail. You can show when the expense was approved, which department accepted it, and when cash left the bank.

When restricted funds change the answer

Suppose your program director attends a grant-funded training event. The reimbursement may look like a simple travel repayment, but the accounting needs more precision than that.

You need to identify:

- Which fund pays it: General operations or a specific restricted fund

- Which function it serves: Program, management, or fundraising

- Which grant or project bears the cost: Especially important for fiscal sponsorship and school-based programs

- What documentation ties it back to donor intent: Agenda, approval, and coding support

If a youth ministry coordinator in a church buys supplies for a donor-restricted outreach event, that reimbursement should land in the outreach fund, not in a generic office supply bucket. If a school administrator incurs travel tied to a funded literacy initiative, it shouldn't disappear into broad administrative travel.

Mileage, travel, and small purchases

Mileage and travel reimbursements often create the most follow-up because people submit them late or without enough support. You need a date, destination, business purpose, and fund coding before approval. For mileage specifically, a standard form keeps everyone consistent. This mileage report resource is the kind of document that prevents later confusion.

QuickBooks can help smaller organizations with basic accounting, and many nonprofits know it well. But class-based tracking often requires extra manual cleanup when reimbursements touch multiple funds, grants, or functional categories. That's where true fund accounting systems have an advantage.

Reimbursement expense isn't just about paying someone back. It's about proving the right mission dollars paid the right mission cost.

The Fund Accounting Behind Reimbursements

The test of a reimbursement expense process is whether it holds together from policy to journal entry to external reporting. That's where many organizations feel strain, especially if they're using a mix of spreadsheets, email approvals, and accounting software built for commercial businesses first.

A reimbursement should reduce or record expense in the right place. It should not create accidental income, inflate grant revenue, or muddy your Statement of Functional Expenses.

The mistake that distorts nonprofit reports

A common accounting error is treating reimbursement-related funds as revenue when they are really offsetting costs. A common error among small nonprofits is incorrectly classifying reimbursement funds as revenue, which inflates income and distorts the Statement of Functional Expenses. The correct method is to credit the expense account, effectively reducing the cost.

That sounds technical, but the practical impact is simple. If your books overstate revenue and leave expenses in the wrong function, your Form 990 tells an inaccurate story about how resources were used.

For a deeper look at the accounting structure underneath this, this guide to fund accounting for nonprofits is a helpful companion.

What an auditor expects to see

Auditors usually aren't looking for fancy reimbursement workflows. They're looking for consistency, support, and evidence that your policy governs practice.

Non-negotiable items include:

- Written policy: It should define reimbursable costs, approval levels, timelines, and exceptions.

- Business purpose support: A receipt alone isn't enough if no one can explain mission relevance.

- Approver separation: The person requesting the reimbursement shouldn't approve their own request.

- Fund and function coding: Every reimbursement should land in the correct fund and functional area.

- Clear payment trail: Finance should be able to tie approval, entry, and payment together.

- Exception handling: Missing receipts and unusual requests need documented review, not hallway conversations.

Why generic tools create extra work

QuickBooks is familiar, and that matters. Aplos is often considered by churches and faith-based groups because it speaks nonprofit language. Blackbaud has deep fundraising history and strong donor records for larger teams. Bloomerang is respected for donor engagement, and Kindful built loyalty around simple CRM use before its transition into broader platforms.

Those tools all have strengths. The gap usually appears when reimbursement expense touches multiple operating areas at once. Accounting sits in one place, donor restrictions in another, volunteer activity in another, and marketing or event context somewhere else. Staff then bridge the gaps manually.

That manual bridge is where coding errors, duplicate entries, and functional expense confusion tend to begin.

Building Your Internal Controls and Policy

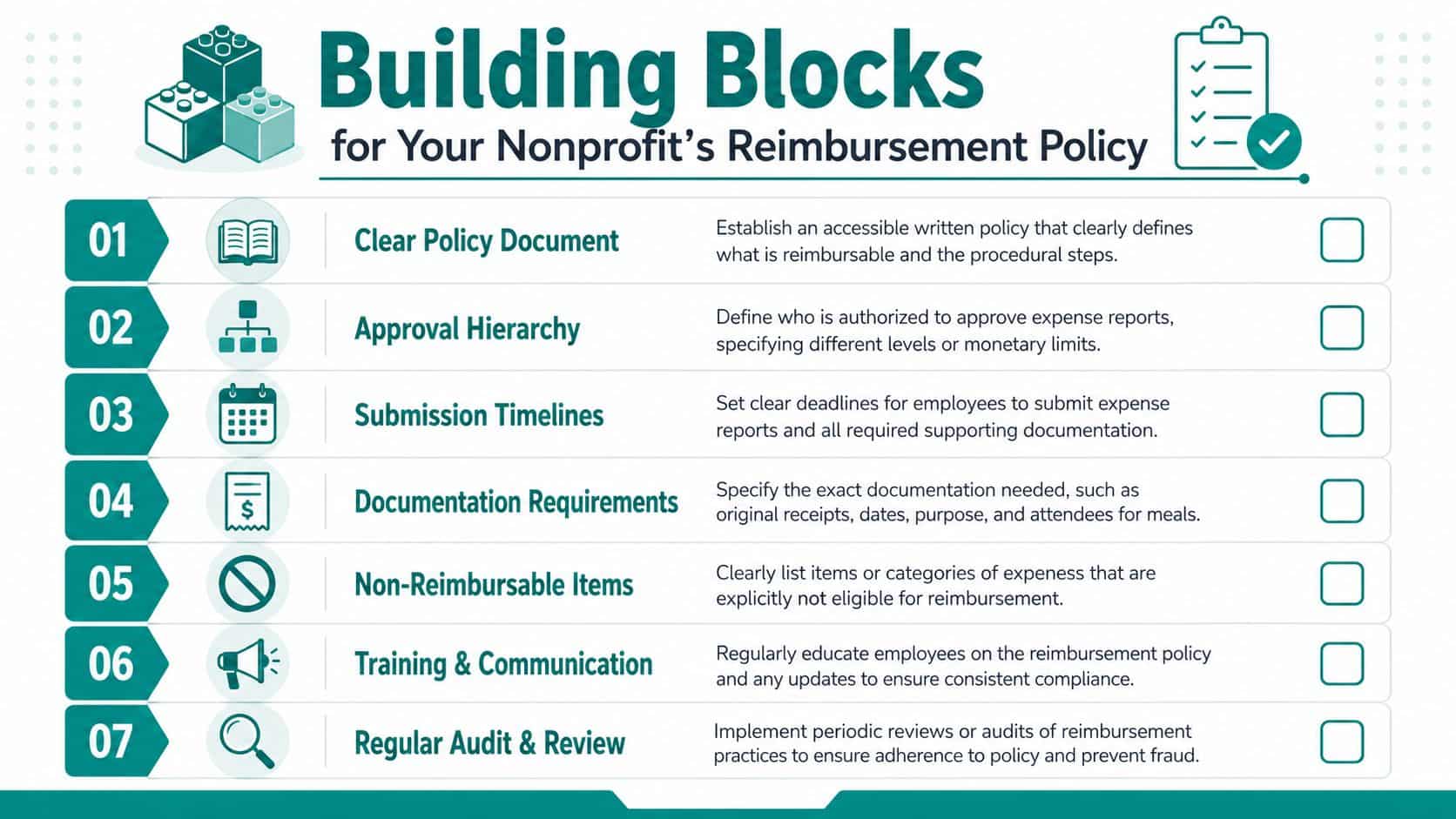

A reimbursement expense policy does its best work before anyone spends money. It sets expectations early, makes approvals predictable, and gives finance something solid to enforce when requests come in incomplete.

The most important control is usually the least popular one. Deadlines. If people know the organization takes timing seriously, submission habits improve fast.

The deadline that changes tax treatment

Under IRS accountable plan rules, reimbursements submitted more than 90 days after the expense was incurred automatically become taxable income to the employee, requiring the organization to process it as wages. That's not a minor paperwork issue. It changes payroll treatment and creates avoidable frustration for staff.

Related IRS guidance also states that reimbursements are excluded from taxable income if the employee substantiates the expense within 60 days under accountable plan rules, as confirmed in IRS Publication 463.

What your policy should say in plain English

Your team doesn't need a legal memo. They need simple instructions they can follow without guessing.

A workable policy should cover:

- Who may request reimbursement: Employees, approved volunteers, ministry leaders, project leads, or school staff

- What counts as reimbursable: Travel, supplies, approved meals, software, training, and other mission-related costs

- What support is required: Itemized receipts, mileage logs, dates, business purpose, and attendees for meals when relevant

- Who approves what: Direct supervisor first, then finance, with board review for executive reimbursements

- When requests are due: A firm internal deadline that protects tax treatment and month-end close

- What happens if the request is late: Payroll treatment, exception review, or denial based on policy

From receipt to Form 990

A reimbursement request doesn't stop at repayment. Once posted, it affects your expense classifications and eventually the figures behind your Form 990.

If a program meal gets miscoded as administration, your program expense totals fall and your administrative totals rise. If a grant-funded training reimbursement lands in unrestricted operations, restricted fund reporting goes off course. If reimbursement-related offsets are booked as revenue, the Statement of Functional Expenses becomes distorted.

Board-level concern: Sloppy reimbursement coding can make a healthy program look less mission-focused than it really is.

This is why reimbursement expense belongs inside your internal control conversation, not just your accounts payable process. If you need a starting framework, a reimbursement policy template for clubs and member groups can be adapted for nonprofits, churches, and school programs.

How AlignMint Simplifies Expense Compliance

The old way is familiar. Someone buys supplies, emails a receipt, finance downloads it, enters data by hand, asks which fund should be charged, then follows up again because the receipt isn't itemized. Nothing is technically impossible. It's just slow, easy to miss, and hard to review later.

The better approach is to make the system enforce the policy.

Before and after the spreadsheet method

Before, reimbursement expense lives in fragments. Approval is in email. Fund coding is in a spreadsheet. Accounting is in one system. Donor context sits in a CRM. Volunteer or event details live somewhere else. Every handoff creates another chance to lose the thread.

After, one request carries the full story. The submitter adds the receipt from a phone, selects the program or fund, and sends it into a defined approval path. Finance reviews exceptions instead of rebuilding context.

That difference matters for more than accounting. It helps church leaders separate ministry costs by fund. It helps schools tie travel and materials back to grants. It helps fiscal sponsors keep each sponsored project distinct. It helps development and finance work from the same donor and fund picture.

What automation should actually do

Good automation doesn't replace judgment. It removes repetitive cleanup and keeps records connected.

What works well in practice:

- Receipt capture at submission: Fewer missing documents later

- Approval routing by role or threshold: The right person sees the right request

- Direct fund and program coding: Expenses land where they belong the first time

- Shared visibility across teams: Finance, program staff, and leadership see the same record

- Connected reporting: The reimbursement flows into accounting and related nonprofit reports without re-entry

Some organizations patch this together with separate tools. QuickBooks may handle accounting, Bloomerang may handle donor records, SignUpGenius or another volunteer tool may track service, and Mailchimp may handle communications. Each tool may be good at its own task. The issue is the handoff between them.

With an all-in-one approach, reimbursement data can sit alongside donor management, volunteer management, events, online giving pages, team communication, and marketing. That gives leadership a more complete picture, especially when a reimbursement expense needs to be understood in the context of a campaign, a grant, or a volunteer-led event.

Why nonprofit leaders care about this

You don't buy software to admire features. You want fewer exceptions, cleaner books, and faster answers.

That's why AI is becoming useful when it's grounded in your actual nonprofit records. A tool like Minty AI can help answer practical questions about spending patterns, fund balances, or grant activity without exporting data into another spreadsheet. And if your organization is small, pricing matters too. A free tier for nonprofits under $100K and plan-based user allowances (1 on Free, up to 10 on Plus, up to 25 on Pro, and unlimited on Enterprise) removes a common barrier to getting everyone into the same system.

If you want to see how a connected workflow handles approvals, payments, and audit support, these reimbursement workflow details show what that looks like in practice.

Your Reimbursement Processing Checklist and Next Steps

A good reimbursement expense process is simple enough for staff to follow and strict enough for auditors to respect. That balance is what keeps month-end calmer and donor reporting cleaner.

Print this checklist. Hand it to your team. If a request misses one of these steps, send it back before it reaches accounting.

A practical checklist you can use

-

Confirm the business purpose Make sure the expense directly supports your operations, program work, school activity, church ministry, or approved grant.

-

Collect support at the time of spending Require receipts, mileage logs, dates, and a short note explaining why the expense was necessary.

-

Check the deadline before approval Late requests create tax and payroll issues that are harder to fix after the fact.

-

Code the right fund and function Decide whether the expense belongs in program, administration, or fundraising, and which fund should bear it.

-

Follow the approval chain Keep supervisor review and finance review separate. Escalate executive reimbursements appropriately.

-

Record the journal entry correctly Book the expense and liability first, then clear the liability when payment is made.

-

Review reporting impact Make sure the reimbursement flows properly into internal statements and the records supporting Form 990.

-

Retain the audit trail Keep the request, support, approvals, coding, and payment record together.

One last practical note

Travel allowances and supporting records can be especially confusing when teams work across jurisdictions or compare policies from different countries. For a helpful international perspective on documentation exceptions, Baron Tax and Accounting's overview of ATO exceptions for travel allowance expenses is worth reading.

If you're done with disconnected tools, start by tightening the policy and standardizing the form. Then move the process into one system that can carry the reimbursement from receipt to journal entry to final report without manual rework.

You can also explore our all-in-one accounting features, read more about nonprofit internal controls, or revisit fund accounting basics.

AlignMint brings reimbursement expense into the same place as your accounting, donor management, volunteers, events, marketing, and team communication. If you want true fund accounting, built-in CRM and marketing tools, Minty AI, plan-based user allowances (1 on Free, up to 10 on Plus, up to 25 on Pro, and unlimited on Enterprise), and a free plan for nonprofits under $100K, visit AlignMint and see whether one connected system can replace the spreadsheets and side tools you're still managing.

Ready to try AlignMint with your nonprofit?

Start free — set up donor tools, giving pages, and Minty AI. Upgrade when you need accounting.