For related tools, see Alignmint features.

Fund Accounting: A Nonprofit Leader's Guide to Clarity

Quick Answer: Fund Accounting: A Nonprofit Leader's Guide to Clarity

Fund accounting tracks money by purpose so you know what is available to spend without breaking donor or grant restrictions. It works when revenue enters the right fund on day one, shared costs have clear allocation rules, and fund balances stay visible for daily decisions, not just year-end reporting.

You know the feeling. The board packet is due, the bank balance looks healthy, and yet you still can't answer one simple question with confidence. What can we spend right now without stepping on a donor restriction or grant condition?

That uncertainty wears people down. Fund accounting solves it, but only when you treat it as a daily operating system, not just a year-end reporting method. This guide shows how to make fund accounting practical, readable, and useful for real decisions.

End the Financial Guesswork for Good

A lot of executive directors live with a quiet financial tension. The checking account says one thing. The grant files, campaign promises, and program needs say something else.

That gap is where bad decisions happen. A team hires too early, approves a purchase from the wrong pool of money, or tells a program lead that funds are available when they aren't.

The problem isn't the bank balance

The bank balance is only part of the story. In a nonprofit, cash can be sitting in the account and still be spoken for. A grant may cover one program. A donor gift may be set aside for a capital need. A board-designated reserve may be untouchable unless leadership makes a formal decision.

Most public explainers stop at compliance. But Aplos notes that most explainers frame fund accounting as a static bookkeeping concept, while its real power is providing real-time balances for operational control.

When finance teams can see current fund balances after allocations and shared costs, they stop guessing and start leading.

This is the essential value. You aren't just producing cleaner statements for the auditor. You're giving yourself a reliable answer before the board meeting, before the hiring decision, and before you promise a new service to the community.

What confidence looks like

When fund accounting is working, your finance conversations get simpler.

- Board questions get clearer answers: You can say what remains in a grant or campaign fund without opening three spreadsheets.

- Program leaders make better requests: They know which dollars are flexible and which are committed.

- Cash planning gets safer: You stop confusing cash on hand with money available for general use.

I've seen leaders carry too much stress because their reports were technically complete but operationally weak. They could close the month, but they couldn't tell what was free to spend today.

That's the difference this guide addresses.

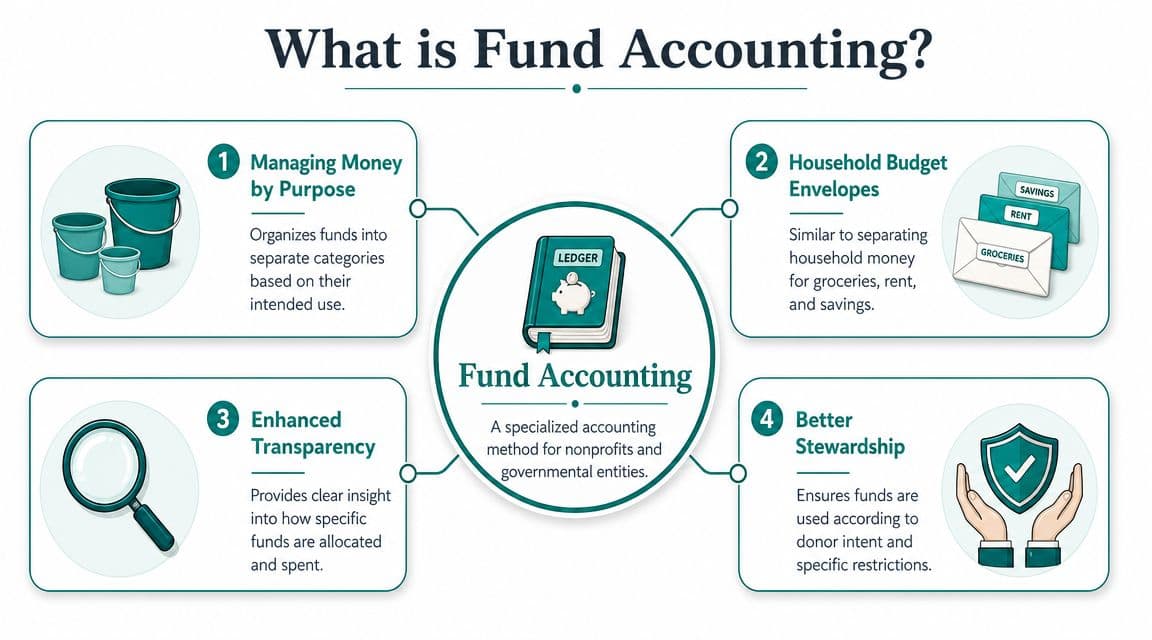

What Is Fund Accounting Really

Fund accounting means organizing money by purpose. Instead of treating every dollar as one general pool, you track separate pools of resources based on how they may be used.

For a nonprofit, that structure isn't a nice extra. It's how you preserve trust.

Think in envelopes, not one pile

The easiest way to explain it is with envelopes. You wouldn't put rent, groceries, and savings into one envelope and hope you'll remember what belongs where. You'd separate them because each has a purpose.

Fund accounting does the same thing for your organization. It helps you track operating support, grants, designated gifts, and program resources without blurring them together.

Foundant explains that fund accounting lets a nonprofit use a single chart of accounts to track multiple funds. That means you can keep money segregated for reporting and still pull an income statement for each fund, without separate bank accounts for every source.

If you want a simple terminology reference, Alignmint's fund accounting glossary gives a useful baseline.

Why nonprofits need a different logic

Business accounting asks whether the organization earned a profit. Nonprofit accounting asks whether the organization honored restrictions, matched spending to purpose, and can explain what happened.

That's why fund accounting is so common in nonprofits and government. Berkeley's guidance and Foundant both describe it as a system built around tracking money allocated to different operations rather than treating all resources as owner equity. In plain terms, it fits organizations that answer to donors, grantmakers, boards, and the public.

Practical rule: If a donor, grantor, or board would expect a separate answer about how money was used, that activity probably belongs in its own fund view.

For faith-based organizations, this matters even more. Churches often receive a mix of general tithes, missions giving, building funds, and designated gifts. If that's your world, this guide to managing restricted funds in churches is worth reading because it stays close to the actual decisions pastors and administrators face.

What works and what doesn't

A healthy fund accounting setup does a few things well:

- It separates intent from convenience: You don't spend from the easiest account. You spend from the right fund.

- It keeps one accounting structure readable: You don't create separate books every time a new grant arrives.

- It supports decision-making: You can see how a fund is performing, not just whether the general ledger balances.

What doesn't work is calling something fund accounting when it's just tagging transactions after the fact. If your team still needs side spreadsheets to know what remains in a restricted gift, the structure hasn't done its job.

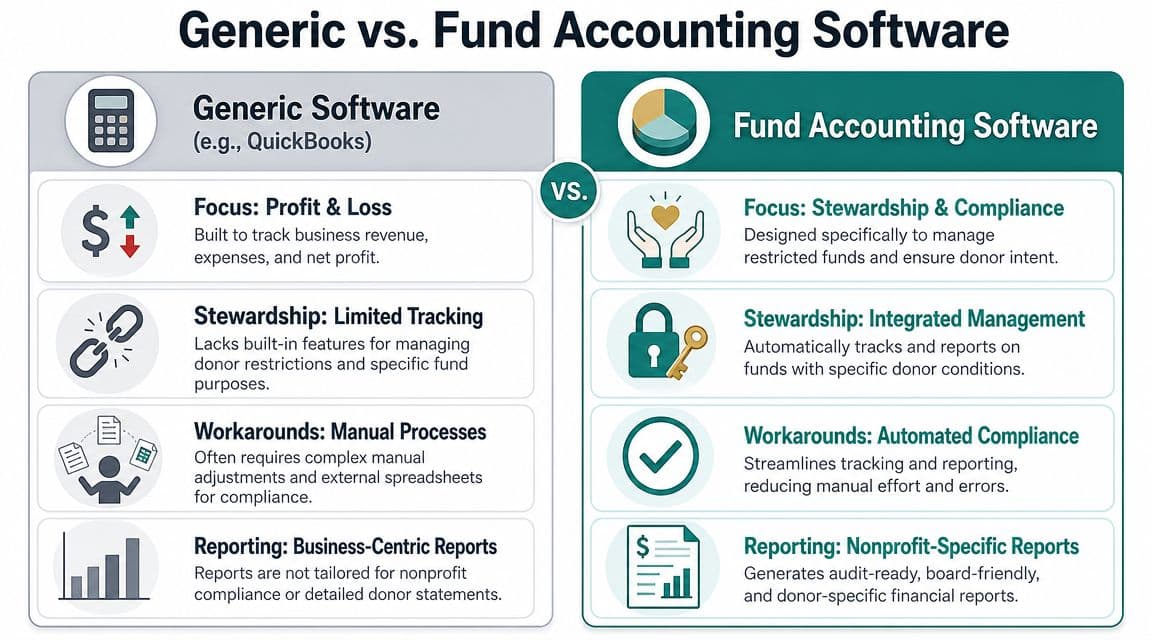

Why Generic Software Puts Your Mission at Risk

QuickBooks is familiar. That's a real advantage. Many nonprofits start there because the interface is known, the accountant knows it, and it handles standard bookkeeping well.

The problem is that familiarity can hide a mismatch. QuickBooks was built for businesses tracking profit and loss. Nonprofits need stewardship by fund.

Where the workarounds start

Most nonprofits using generic software rely on classes, locations, spreadsheets, or manual journal entries to imitate fund tracking. That can work for a while.

Then the organization grows. A grant has payroll, indirect costs, and shared expenses. A board member asks what's left in one restricted fund after those allocations. The answer lives partly in the accounting file, partly in a worksheet, and partly in one staff member's memory.

That is fragile.

If you're comparing options, this review of tools better than QuickBooks for nonprofits lays out the practical differences.

The real risk is false confidence

Generic software can produce reports. That's not the same as producing the right reports at the right level of clarity.

Blackbaud emphasizes that the core technical control in fund accounting is fund segregation, where each resource pool is tracked separately to prove spending matched donor or grantor intent. If that separation depends on manual discipline rather than the accounting structure itself, mistakes become much easier.

Often, the following breaks first:

| Issue | What happens in generic software |

|---|---|

| Restricted balance visibility | Staff rely on exports or custom spreadsheets |

| Shared cost allocation | Payroll and overhead get posted late or unevenly |

| Board reporting | Reports need translation before non-finance leaders can use them |

| Staff transitions | Knowledge sits with one bookkeeper or outside accountant |

Competitors do some things well, but not this natively

QuickBooks is strong for standard small-business bookkeeping. That's why so many organizations begin there. The gap is not that it fails at accounting. The gap is that it doesn't natively model nonprofit funds the way a mission-driven finance team needs.

The same caution applies when a CRM and accounting stack are loosely connected. You may have a donor gift in one tool, the deposit in another, and the restriction detail somewhere else. That split creates reporting lag.

If your finance team can explain a fund only after exporting data, the system is giving you records, not control.

A true fund accounting platform treats restricted, unrestricted, grant, and program activity as accounting structure from the start. That reduces cleanup work and makes the answer available before month-end scramble begins.

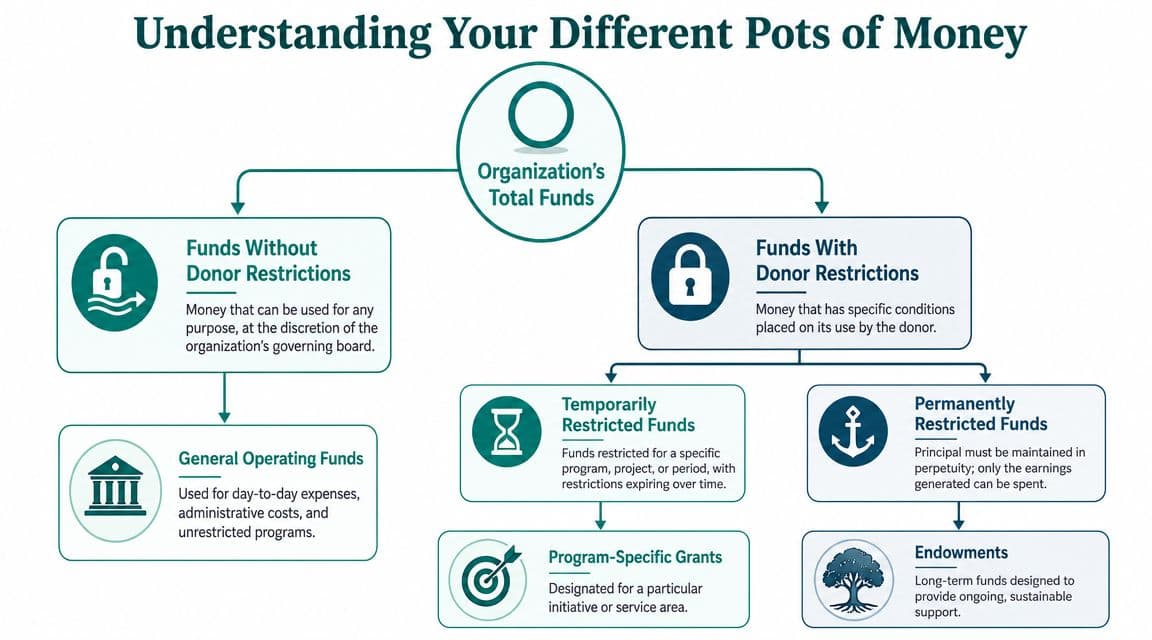

Understanding Your Different Pots of Money

Once you stop looking at cash as one pool, the next step is naming the pools clearly. Such an approach often initiates many reporting headaches. Teams use the same words differently, or they mix legal restrictions with internal preferences.

You need a simple vocabulary that everyone can follow.

Start with the big divide

The most important distinction is between funds without donor restrictions and funds with donor restrictions.

Funds without donor restrictions are your most flexible resources. They support operations, administration, staffing gaps, and mission needs that don't have outside limits attached.

Funds with donor restrictions come with conditions. The donor or grantor has limited how the money may be used, or when it may be used, and your records need to preserve that distinction.

Common categories you should name clearly

A practical chart of funds usually includes categories like these:

- Operating funds: Your day-to-day unrestricted money.

- Program funds: Resources tied to a specific service area, such as food pantry, after-school, or outreach work.

- Grant funds: Each major grant often needs its own tracking logic.

- Capital funds: Building work, equipment campaigns, or facility improvements.

- Endowment-related funds: Resources where principal is meant to remain intact and only earnings are available to spend.

If you're revisiting your structure, a nonprofit chart of accounts template can help you map the categories without overcomplicating them.

Restriction type and operating use are not the same thing

This is the point that trips up a lot of teams. A fund can be restricted by donor intent and still also relate to a specific program or campaign. Those are different lenses.

One lens answers, "Can we legally or ethically spend this on anything else?" The other answers, "What area of work does this support?"

A clean setup separates restriction status from management reporting. If those ideas get mixed together, your reports confuse everyone.

For example:

- A literacy grant may be with donor restrictions and also belong to your education program.

- Your general fund may be without donor restrictions and still be split internally for board review between operations and strategic reserves.

- A building gift may be restricted for capital purposes even if it sits in the same bank account as unrestricted cash.

Keep the structure simple enough to maintain

I've seen organizations create so many funds that no one can post a transaction without asking for help. I've also seen teams keep things so broad that they can't answer basic questions.

The middle ground works best. Build enough fund detail to support stewardship, grant reporting, and board decisions. Don't create a new fund for every passing idea or short-lived event unless you know you'll need to report on it.

A good test is this: if a board member, donor, grantor, or auditor would reasonably expect a separate explanation, create a clear way to track it. If not, keep the structure lean.

Get Reports Your Board Can Actually Understand

The payoff from fund accounting is not technical elegance. It's clarity. Your board should be able to look at a report and understand what money came in, what was spent, and what remains by purpose.

When that works, meetings change. Instead of debating whether the numbers are reliable, leadership can discuss what to do next.

Reporting becomes easier when the structure is right

Sage explains that fund accounting is designed to directly support nonprofit compliance requirements, including IRS Form 990. That's one reason it remains central to audit readiness and transparent stewardship.

But the same structure that supports Form 990 also helps with routine board reporting. If revenue and expenses are coded to the right funds from the start, your statements become easier to read and defend.

A practical example is an income statement by fund. This kind of report helps boards see activity in a format that matches how nonprofits operate.

The reports that matter most

Most organizations don't need more reports. They need a few reports that answer the right questions.

- Statement of Activities by fund: Shows revenue and expense by purpose, not just in total.

- Restricted balance reporting: Shows what remains available within each restricted pool.

- Functional expense reporting: Helps separate program, management, and fundraising costs.

- Grant spending views: Lets staff compare budget, actuals, and remaining balance.

These reports matter because they connect stewardship to action. A board can see whether a program is fully funded, whether unrestricted money is carrying too much overhead, and whether a grant is nearing its spending limit.

Plain-English questions matter too

For many executive directors, the primary obstacle isn't accounting theory. It's report access. You may not want to click through ten filters just to answer a program question.

This is one place where an all-in-one platform can help. Alignmint combines accounting, CRM, volunteers, events, and marketing in one system, and its Minty AI assistant can answer questions against your actual data. That kind of setup is useful when you want finance, fundraising, and operations looking at the same picture.

Board-friendly reporting doesn't mean dumbing things down. It means presenting the truth in a form people can act on.

The strongest reports don't impress anyone with complexity. They reduce anxiety, speed up decisions, and keep the room focused on mission.

Putting Fund Accounting into Practice

Good fund accounting depends less on theory than on habits. The right setup makes those habits easier to keep.

At the center of it all is fund segregation. Blackbaud describes this as the core technical control in nonprofit fund accounting, because each resource pool must be tracked separately to prove spending matched donor or grantor intent.

Build your structure before the pressure hits

Don't wait until audit prep or grant reporting to define your funds. Set them up before the money starts moving.

A workable process usually looks like this:

-

List your recurring money types Include operating support, major grants, programs, capital needs, and any board-designated funds.

-

Create a chart of funds that reflects real management needs If a fund needs separate reporting, separate approval, or a separate balance review, name it clearly.

-

Set posting rules early Revenue should enter the correct fund on day one. Expenses should be coded to the fund that benefits from them.

-

Define allocation methods for shared costs Payroll, occupancy, and common services need a consistent method. Don't invent it at year-end.

If your team needs a practical reference for setup and daily handling, this guide to restricted funds is a good operational starting point.

Daily discipline matters more than heroic cleanup

The strongest finance teams don't rely on one person who can untangle everything later. They reduce the need for cleanup.

That means a few controls have to be essential:

- Approval separation: The person requesting spending shouldn't be the only person deciding how it is coded.

- Transaction-level coding: Every receipt, bill, deposit, and journal entry needs the right fund logic attached.

- Regular reconciliation: Fund balances should be reviewed routinely, not just when a report deadline appears.

Real-time visibility changes management behavior

This is the part most organizations miss. Fund accounting is often treated like a filing requirement. In practice, it's an operating control system.

When balances stay current, you can answer questions like these without delay:

| Management question | What strong fund accounting gives you |

|---|---|

| Can we afford this program expense? | A current view of the related fund balance |

| Is this grant overspent? | Spend-to-date against the correct resource pool |

| What can leadership reallocate? | Clear distinction between flexible and committed money |

That visibility also improves relationships across departments. Program leaders stop seeing finance as the team that says no. Finance becomes the team that can say yes, no, or not yet, with a reason everyone understands.

Your Checklist for a Clearer Financial Future

A finance crisis rarely starts with fraud or a failed audit. More often, it starts in a board meeting when someone asks a simple question. How much of this cash can we use? If your team needs three spreadsheets, two inbox searches, and a follow-up meeting to answer, the problem is not effort. It is structure.

The fix is a practical one. Build a setup that shows what is available, what is committed, and what needs attention before a deadline forces the issue. Fund accounting earns its keep here. It turns fundraising promises into current operating facts, which is what leaders need when staffing, spending, and reporting decisions cannot wait.

A simple plan you can act on

-

Reduce spreadsheet risk Keep spreadsheets for analysis if they help. Do not let them remain the only place restricted balances, grant timelines, or board-designated reserves make sense.

-

Map the funding structure you manage List the funds, grants, programs, campaigns, reserves, and special projects your team uses to make decisions. Remove categories that only exist because an old report needed them five years ago.

-

Test whether your software handles fund logic directly If accurate answers depend on exports, workarounds, or side calculations, month-end will stay heavier than it should be and day-to-day decisions will stay slower than they need to be.

-

Connect fundraising records to accounting records Revenue details should not stop with the development team. When gifts and restrictions flow into the accounting system cleanly, finance can verify balances faster and leadership can act with more confidence.

-

Choose a system people will use The strongest setup is not the one with the longest feature list. It is the one that finance, development, and program staff can use consistently enough to keep records current and reports credible.

Software choice matters because the trade-off is real. A generic tool can look cheaper at first, then cost the team hours every month in recoding, reconciliations, and explanation. A purpose-built system usually asks for more upfront discipline in setup, but it gives leaders a clearer read on what money is available. Alignmint was built around that reality, including a free tier for nonprofits under $100K and plan-based user allowances (1 on Free, up to 10 on Plus, up to 25 on Pro, and unlimited on Enterprise), so the people raising money and the people stewarding it are not working from different versions of the truth.

Clear books lower stress. They also help you approve spending with confidence, explain fund balances without hesitation, and walk into the next board meeting ready for the questions that matter.

Related guides

- Fund accounting for nonprofits — nonprofit-specific primer on restricted funds and reporting

- Fund accounting software — buyer guide for nonprofit accounting platforms

- Fund accounting feature — how Alignmint connects finance, donors, and programs

Ready to try Alignmint with your nonprofit?

Start free — set up donor tools, giving pages, and Minty AI. Upgrade when you need accounting.