For related tools, see Alignmint features.

Nonprofit Fiscal Sponsor: A Director's Practical Guide

Quick Answer: Nonprofit Fiscal Sponsor: A Director's Practical Guide

A nonprofit fiscal sponsor carries legal responsibility for charitable funds raised on a project's behalf while providing accounting, oversight, and shared back office. It is not a pass-through account. Strong arrangements name the sponsorship model upfront, define spending approvals, and track restricted gifts by project so directors can report with confidence.

You may be staring at a promising new program, a founder with momentum, and a spreadsheet that already feels fragile. That's usually the moment fiscal sponsorship stops being a legal idea and becomes a finance problem.

A nonprofit fiscal sponsor can help a project raise tax-deductible gifts quickly and operate under experienced oversight. The hard part isn't defining the model. It's setting up accounting, restricted funds, approvals, and reporting in a way that stays compliant when real money starts moving.

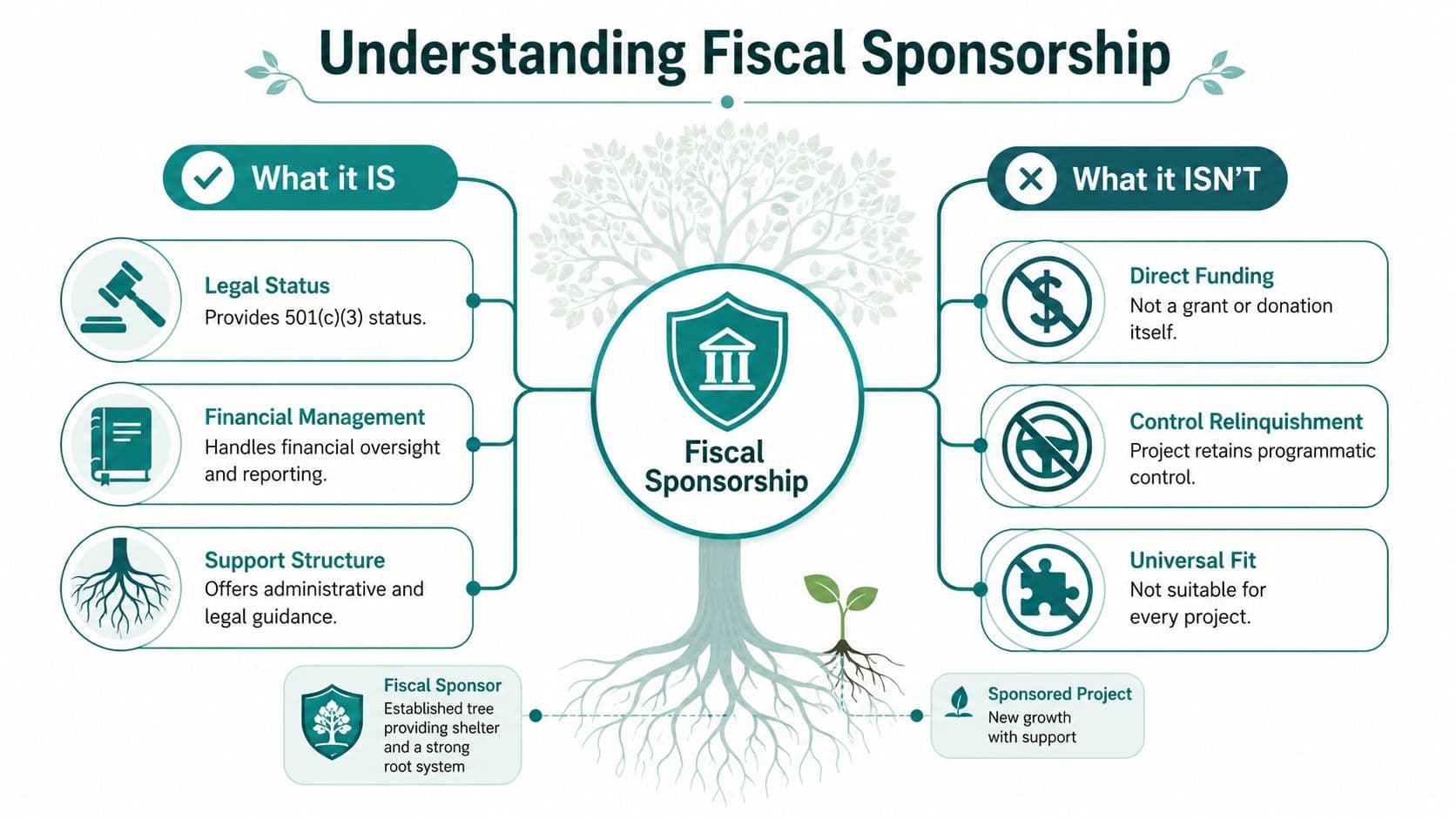

Understanding Fiscal Sponsorship at Its Core

A nonprofit fiscal sponsor is a bit like a mature tree sheltering new growth. The project gains cover, credibility, and a root system for finance and administration, while the sponsor carries legal responsibility for how charitable funds are received and used.

That shelter is valuable because it lets a project accept tax-deductible donations under the sponsor's charitable status. It also gives funders confidence that someone with established governance, accounting, and oversight is watching the details that often trip up early-stage work.

What a sponsor is actually providing

At its best, fiscal sponsorship is shared infrastructure. A recent field scan reported that 100 participating fiscal sponsors collectively managed more than $2.6 billion in community investments in the previous year, showing that this is no side arrangement but a meaningful operating model in the sector, as reported by Social Impact Commons.

That matters because many leaders still picture sponsorship as informal. In practice, strong sponsors provide finance, HR, legal coordination, insurance oversight, and risk management, while the project focuses on mission delivery.

If you want a quick baseline definition, Alignmint's fiscal sponsor glossary entry is a useful starting point.

A healthy sponsorship arrangement gives the project room to lead its work, but it does not remove the sponsor's duty to supervise charitable funds.

What fiscal sponsorship is not

It is not a grant by itself. It is not a shortcut around internal controls. And it is not a clean fit for every initiative.

Three misconceptions cause trouble fast:

- It's not a pass-through account: Donors are giving to the sponsor for a charitable purpose, not parking money for someone else to spend freely.

- It's not total project independence: The project may lead programs, but the sponsor still sets financial guardrails.

- It's not always temporary: Some projects eventually spin out. Others remain under sponsorship because the arrangement keeps overhead and administration manageable.

For directors, the practical question is simple. Are you offering or receiving real administrative stewardship, or are you just trying to move money faster. If it's the second one, the arrangement is weak before the first gift arrives.

The Common Fiscal Sponsorship Models Explained

The model you choose shapes who employs staff, who signs contracts, who owns risk, and how money is tracked. Most confusion comes from letter labels. Directors usually need plain language instead.

The comprehensive model

In the full model, the project operates as part of the sponsor itself. Staff may be employees of the sponsor. Contracts often sit with the sponsor. Financial activity is fully inside the sponsor's books.

This model can work well when the project is early, the sponsor wants tighter oversight, or the work carries enough legal or employment risk that fragmented responsibility would be unwise. It usually gives the sponsor the most control, but it also asks the sponsor to carry the most direct operational burden.

The upside is clarity. The downside is that the project may feel less autonomous than its leaders expected.

The grant relationship model

Model C, often called the pre-approved grant relationship, keeps more separation between sponsor and project. The project is usually its own entity, or at least functions with more distinct identity, while the sponsor receives charitable funds and then makes grants to support approved charitable work.

According to the Johnson Center's review of the Fiscal Sponsor Directory, 63% of listed sponsors used Model C, which makes it the most common structure among listed participants. Their discussion of fiscal sponsorship models and directory data is worth reading if you want the sector context.

That popularity makes sense. Model C often appeals to sponsors that want clear separation, and to projects that want more day-to-day independence without giving up access to charitable fundraising.

For a more accounting-focused look at the operational differences, this guide on fiscal sponsorship accounting models is helpful.

A practical comparison

| Model | Best fit | Main advantage | Main pressure point |

|---|---|---|---|

| Comprehensive | Early-stage or high-oversight projects | Clear sponsor control and integrated operations | More sponsor workload and liability |

| Grant relationship | Projects wanting more independence | Cleaner separation between entities | Requires disciplined grant review and documentation |

Where directors get tripped up

The legal form should match the actual workflow. If the sponsor is hiring people, approving expenses, and carrying insurance exposure, a loose agreement that pretends the project is mostly independent creates confusion.

If the project has its own leadership and operations, but the sponsor still receives donations, then the grant relationship model often fits better. Even then, the sponsor can't step back from oversight. It must review, approve, and document how funds support charitable purposes.

Decision rule: Choose the model that matches who controls staff, contracts, spending approvals, and compliance work in real life, not the model that sounds simplest in a pitch meeting.

Evaluating the Benefits and Risks for Both Sides

Fiscal sponsorship can be an excellent arrangement when expectations are realistic. It can also sour quickly when one side thinks it bought flexibility and the other thinks it retained full authority.

What the project gains and gives up

For a project, the obvious gain is speed. You can start fundraising and operating under an established charitable umbrella instead of building every back-office function from scratch.

You also gain credibility. Donors, grantmakers, and vendors often feel more comfortable when an established nonprofit is handling gift processing, reporting, and governance.

But there is a cost. The project won't have complete freedom over how funds are held, approved, or described. That can feel frustrating to founders who are used to making decisions quickly.

Common trade-offs for projects include:

- Faster fundraising: Gifts can be received through the sponsor's charitable status.

- Less administrative strain: The sponsor may take on accounting, reporting, and compliance tasks.

- Lower autonomy: Spending requests, contract reviews, and public messaging may need sponsor approval.

- Fee pressure: Administrative fees are normal and should be expected, not resented after the fact.

What the sponsor gains and risks

For sponsors, the upside is mission expansion. You can support promising work without launching each idea as a separate corporation, separate board, and separate finance office.

There can also be earned administrative revenue, but that benefit is often overstated. If your systems are weak, your fee won't cover the staff time needed to untangle restrictions, approvals, payroll questions, insurance issues, and donor reporting.

The risks are more serious than many boards expect:

- Legal exposure: If the project signs bad contracts or mishandles funds, the sponsor may absorb the consequences.

- Reputation spillover: Donors rarely separate the project's failures from the sponsor's judgment.

- Operational drag: Sponsorship can strain finance and leadership teams if intake standards are loose.

- Control tension: Projects may ask for freedom that the sponsor cannot responsibly give.

A side-by-side decision often helps directors think clearly:

| Perspective | Feels attractive when | Becomes dangerous when |

|---|---|---|

| Sponsored project | You need fundraising access and administrative support | You expect unrestricted control over money raised under the sponsor |

| Fiscal sponsor | You want to expand mission impact through shared services | You accept projects without enough staff capacity for oversight |

If you're weighing sponsorship against forming a standalone charity, this comparison of fiscal sponsorship vs 501(c)(3) lays out the structural differences clearly.

The best partnerships start with a shared understanding that sponsorship is not independence with a borrowed tax exemption.

Critical Financial and Legal Responsibilities

Many nonprofit fiscal sponsor arrangements become durable or risky at this point. The legal rule is well known. Most organizations struggle with the accounting consequences.

Discretion and control is not optional

The sponsor must maintain complete discretion and control over contributed funds. Public Counsel's guidance explains that if the sponsor merely acts as a conduit, the arrangement can be challenged and the tax-deductibility of donations can be put at risk. Their primer on fiscal sponsorship and discretion and control is one of the clearest plain-English references on this point.

That requirement sounds legal, but it lands in daily bookkeeping. If gifts come in for Project A, your records need to show that the sponsor received them in its own name, restricted them to the approved charitable purpose, and approved disbursements accordingly.

A weak setup usually has one or more of these habits:

- Project-directed spending: The project treats the bank balance as its own and informs the sponsor after the fact.

- Loose coding: Bookkeepers rely on memo fields or spreadsheets outside the ledger to track restrictions.

- Shared cash without clear fund balances: Staff can't answer what remains available for one project versus another.

- Informal approvals: Expense releases happen by email thread with no durable audit trail.

The accounting gap most guides skip

Many articles stop after saying funds should be kept separate. That's true, but it doesn't solve the operator's problem.

The primary challenge is handling project-level restrictions, balance-sheet presentation, audits, and Form 990 reporting without commingling funds or hiding obligations. This is especially hard when one sponsor manages several projects at once. The Council of Nonprofits discussion of fiscal sponsorship points to the model's practical use as an alternative to starting a new nonprofit, but most day-to-day finance teams still have to build the workflow themselves.

Here's the finance standard I recommend in practice:

- Create a distinct fund structure for each sponsored project. Don't bury project activity in classes alone.

- Record donor restrictions at receipt. Don't wait until month-end to sort intent from email notes.

- Approve expenses against purpose and available balance. Approval should confirm both.

- Report at two levels. Project leaders need project statements. Leadership and auditors need consolidated sponsor reports.

- Review liabilities carefully. If a project has commitments, payroll obligations, or prepaid activity, your balance sheet should surface them clearly.

Practical rule: If your controller can't pull restricted balances by project and then reconcile them to the organization-wide statements without spreadsheet patchwork, your setup is too fragile.

Why generic software often creates avoidable risk

QuickBooks deserves credit. Many nonprofits use it because it's familiar, affordable, and widely supported by outside bookkeepers. For a single-entity nonprofit with modest complexity, it can be serviceable.

But for fiscal sponsorship, classes are often asked to do work they weren't built to do. A class can help label transactions. It does not, by itself, create true fund accounting discipline around restrictions, net assets, grant obligations, or sponsor-level reporting across multiple sponsored projects.

The same caution applies to tools like Xero paired with add-ons. Those stacks can work for some organizations, but they usually require more manual reconciliation and stronger finance staff discipline to keep project restrictions clean.

Purpose-built nonprofit systems are better suited to this structure because they model funds natively. One option is Alignmint's fiscal sponsor compliance checklist, which pairs policy questions with the accounting controls sponsors need. Alignmint itself is an all-in-one platform that combines fund accounting, CRM, volunteers, events, and marketing in one system, with unrestricted and restricted funds modeled directly rather than approximated through class tracking. For directors who are also sorting payroll, HR boundaries, and shared-employer questions, PEO Metrics' nonprofit PEO strategy is a practical companion resource.

What works in the real world

The sponsors that stay out of trouble aren't necessarily the largest. They're the ones that insist on boring discipline.

They document approvals. They keep project balances visible. They don't release restricted funds because a project leader is persuasive. And they don't promise custom reporting their system can't support each month without manual cleanup.

How to Evaluate a Partnership and Structure Your Agreement

Good sponsorship decisions usually happen before the agreement is signed. Bad ones often start with a compelling mission and too little due diligence.

Questions both sides should ask early

If you are the sponsor, start with mission fit and management reality. If the project's work is outside your charitable purpose, or your staff can't supervise it properly, decline early and politely.

If you are the project, ask how the sponsor operates. Don't stop at fees and branding. Ask who approves expenses, how often reports are delivered, how donor restrictions are tracked, and who owns the relationship with funders.

A useful screening list includes:

- Mission alignment: Does the project clearly fit the sponsor's charitable purpose and public commitments?

- Leadership maturity: Can the project lead deliver budgets, reports, and documentation on time?

- Financial discipline: Are there clean records, realistic budgets, and clear spending authority?

- Risk profile: Will the work involve employment exposure, contracts, insurance complexity, or sensitive activities?

- Capacity on the sponsor side: Can current finance and operations staff absorb the added supervision?

Don't confuse a worthy idea with a manageable sponsored project. The first is inspirational. The second is operational.

Terms that should never stay vague

A fiscal sponsorship agreement should answer the questions people avoid during optimistic early conversations. If those answers are fuzzy, the conflict is merely delayed.

At minimum, put these items in writing:

| Agreement area | What should be clear |

|---|---|

| Term and termination | Start date, renewal terms, exit process, and what triggers termination |

| Financial control | How gifts are received, restricted, approved, reported, and disbursed |

| Fees | The administrative fee method and what services it does or does not cover |

| Staffing and contractors | Who hires, supervises, and signs agreements |

| Intellectual property | Who owns program materials, branding, data, and work product |

| Donor and grant relationships | Who communicates with funders and who signs grant reports |

| Wind-down treatment | What happens to remaining restricted funds if the relationship ends |

A strong agreement doesn't signal mistrust. It protects the mission from preventable misunderstandings.

Your Next Steps and Key Resources

A nonprofit fiscal sponsor arrangement works when the legal structure and the accounting structure match. If they don't, you'll feel the strain in approvals, audits, board reports, and donor questions long before anyone uses the word compliance.

Start with your operating reality. Decide how much control the sponsor must hold, what restrictions need tracking, and what reports each audience needs every month. Then test whether your current systems can produce that information cleanly.

For deeper reading, review Alignmint's fund accounting feature overview, its guide to nonprofit accounting software, and its primer on fund accounting for nonprofits. If you're trying to model sponsor fees before you commit, the fiscal sponsor fee calculator is a practical starting point.

The right next step isn't to rush into a sponsorship. It's to pressure-test your controls, your reporting, and your agreement before the arrangement gets busy.

If you're managing sponsored projects and you're tired of stitching together accounting, donor records, volunteer data, events, and marketing across separate systems, take a look at Alignmint. We built it for nonprofit operators who need true fund accounting, clear project reporting, plan-based user allowances (1 on Free, up to 10 on Plus, up to 25 on Pro, and unlimited on Enterprise), and one place to manage the work without adding more software overhead.

Ready to see how Alignmint fits your workflow?

Schedule a free walkthrough — we will help you map donors, funds, and migration steps.